Operating and Financial Leverages

Leverage is a technique used in finance that can improve a company’s asset base, cash flow, and returns but also magnify any losses. Financial and operating leverage are the two most common kinds.

A company can enhance its financial leverage by issuing fixed-income securities or borrowing money from a financial institution. Revenues or profit margins can be amplified through the application of operating leverage by raising revenues or profit margins. Both approaches carry the possibility of failure, but can ultimately be very fruitful for a company.

Financial Leverage

Leverage refers to the use of debt in the financial sector to increase asset holdings or finance activity. Borrowing money is the primary means by which debt is incurred. Borrowers commit to repaying their loan’s original principal plus any accrued interest. Leverage in finance is also known as trading on equity.

Impact of Financial Leverage

Individuals and businesses may use leverage for a variety of reasons. Businesses could be interested in buying new machinery and tools in order to boost their stock price, while private individuals may use borrowing to boost their returns.

In any instance, if the value of the asset improves and the interest rate on the loan is lower than the rate of increase in the asset’s value, the owner of that asset will have a higher return. However, if the value of the assets decreases, it means that the owner will have a higher financial loss.

To keep their earnings growing, companies that use a mix of equity and debt to fund operations need to generate a higher rate of return than the interest rates on their loans. Also, businesses need to demonstrate a readiness to take on debt while keeping their profit margins high.

A higher degree of risk is always present whenever money is borrowed because eventually the borrower or lender will have to pay it back. Regardless of whether or not revenues or cash flows improve, whatever is earned must be applied to debt repayment.

A company’s return on equity (ROE) can be affected either positively or negatively by its use of financial leverage (debt), depending on the inherent risk associated with doing so. With the right amount of financial leverage, a company can maximise its return on equity by taking advantage of the positive relationship between stock price volatility and the level of risk taken. Companies with excessive debt may see their return on equity decline. The goal of financial over-leveraging is to incur massive debt by borrowing large sums of money at a low interest rate and investing them in high-risk ventures.

When the perceived risk of an investment exceeds the anticipated reward, stockholders may reduce their investment in the company.

Implications of Financial Leverage

- Stock Price Volatility

It’s possible that increased financial leverage could cause significant fluctuations in a company’s profits. In turn, this will make it more difficult for employees to keep track of the value of any stock options they may hold in the company, as the stock price will be more volatile. If the price of a company’s stock rises, it will be able to give its investors a larger dividend.

- Bankruptcy

Sales and profits in an industry with few constraints on new entrants tend to swing wildly more often than those in an industry where the barriers to entry are strong. It’s possible that a company’s revenue swings could be the final straw, sending it into insolvency as it struggles to keep up with mounting interest payments and other running costs. In the face of mounting unpaid debts, creditors can petition the bankruptcy court to sell off the company’s assets to recoup their losses.

- Debt availability is restricted.

Creditors look at a company’s leverage while deciding whether or not to provide money. Financial institutions are more hesitant to provide new loans to businesses with a high debt-to-equity ratio due to the increased default risk. However, a highly leveraged corporation will lend out at a higher interest rate to compensate for the higher risk of default if its lenders agree to advance cash to it.

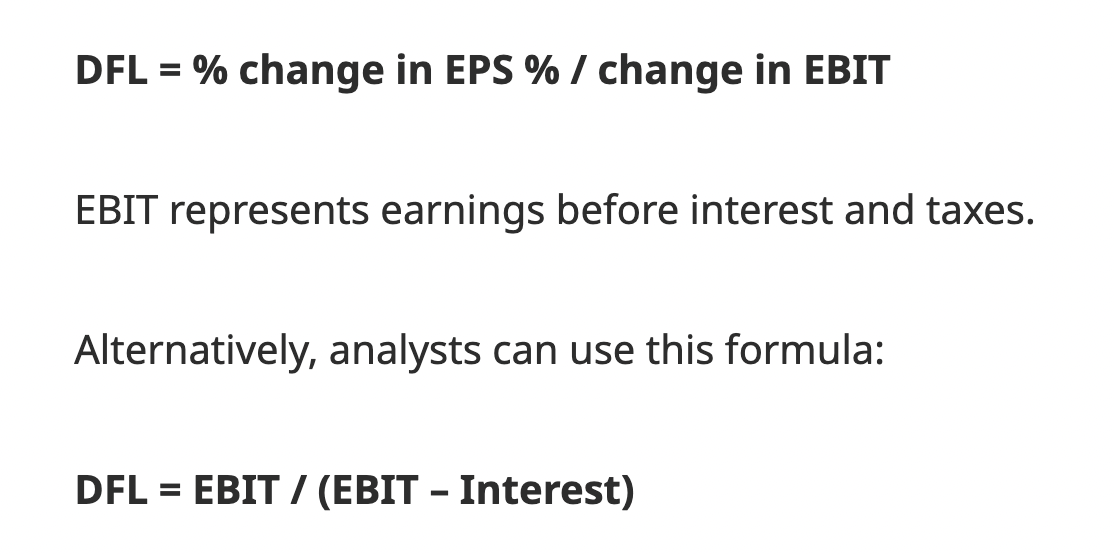

Measuring Financial Leverage

When a business makes adjustments to its capital structure, one way to measure the impact on its operating income is by calculating the leverage ratio, which indicates how much of an impact the shift in operating income has on earnings per share. If a corporation has a significant level of financial leverage, it will see large swings in its bottom line. If the company’s operational income increases, this could lead to exceptional returns.

Operating Leverage

Operating leverage is the relationship between fixed and variable costs. Fixed costs are expenses that are incurred regardless of how many units are sold. Variable costs vary according to sales volume.

A corporation with strong operating leverage has a high fixed cost to total cost ratio, which means that more units must be sold to pay costs. A corporation with poor operating leverage has a high variable cost-to-total-cost ratio, which means fewer units must be sold to pay costs. In general, greater operating leverage results in poorer earnings.

Impact of Operating Leverage

Operating leverage is essentially a cost-benefit analysis of fixed and variable costs. Operating leverage is greatest in businesses with a large share of fixed operating costs versus variable operating costs. This type of business makes more use of fixed assets in its operations. Conversely, organisations with a low fraction of fixed operating costs in relation to variable operating costs have the lowest operating leverage.

The advantages of high operating leverage might be enormous. Companies with high operating leverage can generate more money from each extra sale because they don’t have to increase their costs to make additional sales. When a company picks up, fixed assets like property, plant, and equipment (PP&E), as well as existing employees, may perform a lot more without incurring additional costs. Profit margins grow and earnings rise quickly.

The proportion of land, buildings, plants, and machinery to total fixed costs is higher for a corporation with significant operating leverage. Once these expenses are covered, a rise in sales soon translates into profit. The converse is true if sales decline, however.

On the other hand, if a company has little operating leverage, it means that its variable costs, like those associated with its employees, advertising, and promotion, are more significant. This suggests that a rise in sales will not necessarily result in a rise in operating profit for the company.

Because certain businesses have more substantial fixed costs than others, it is important for investors to analyse the operating leverage of companies operating in the same industry. Companies in the manufacturing sector, for instance, tend to have a larger share of fixed expenses than their service sector counterparts.

If the sales can be estimated properly, then the company’s profitability may be predicted by paying great attention to operating leverage. However, finding a company’s operating leverage can be challenging. Operating leverage is only an estimate because corporations aren’t obligated to publish their per-unit variable costs. In addition, yearly fluctuations can be seen in a business’s price, product mix, and input costs.

Operating Leverage and Its Implications

- Price

The profitability threshold is measured in terms of operating leverage. When the price at which a product is sold is equal to its cost of production, we say that the business is at “break even.”

Operating leverage is critical since it determines how a company sets its prices. A price over the break-even point is required for a profit to be realised. Operating leverage measures the proportion of fixed to variable expenses, and high operating leverage means a greater break-even point. If both companies have similar costs and sales volume, the one with higher operating leverage will need to charge higher prices to break even.

- Sales

Increases in sales are profitable for a company with high operating leverage because the company’s fixed costs do not change. As a result, the corporation benefits from increased sales. When additional output is achieved while maintaining the same level of fixed expenses, this circumstance is referred to as “leveraging fixed costs.” As a result, organisations with higher fixed costs profit from increased sales during these times.

However, when business is slow, these organisations take a hit on every unit sold. Consequently, it might cause even greater financial losses if the business environment is unfavourable.

- Profitability

The degree of operating leverage indicates a company’s cost structure, which is a key component in determining profitability by measuring how sensitive operating income is to a change in revenue streams. Since fixed costs must be paid regardless of sales volume, a business with a lot of them will have a tough time weathering short-term revenue fluctuations. This raises the stakes and, in most cases, results in a lack of flexibility that is detrimental to profits. Companies with a high level of risk and operating leverage have a more difficult time securing low-cost borrowing.

Companies with minimal operating leverage are only slightly affected by shifts in sales revenue. Operating leverage measures how much a company’s profit increases in response to a change in revenue.

Operating leverage increases sensitivity to changes in revenue, and vice versa if fixed costs increase. Operating leverage that is more sensitive to changes in the economy is seen as riskier since it suggests that existing profit margins are less stable over time.

Though riskier, this strategy ensures that every sale made after the point of break-even adds more to the bottom line. A high degree of operating leverage in a cost structure means fewer variable expenses, which in turn means less of a drag on added productivity while simultaneously reducing losses due to low sales.

- Business Risk

Operating leverage can reveal a lot about a company’s risk profile to investors. Although high operating leverage can sometimes benefit organisations, it also makes them subject to abrupt economic and business cycle changes.

As previously indicated, strong operating leverage can boost profit in good times. Companies that have a lot of costs tied up in machinery, factories, real estate, and distribution networks, on the other hand, can’t quickly cut expenditures to respond to a shift in demand. As a result, if the economy suffers a downturn, profits can plummet rather than fall.

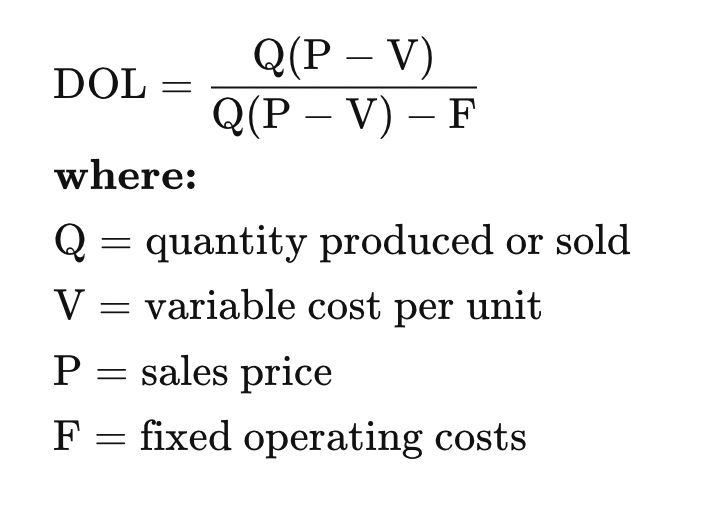

Measuring Operating Leverage

The degree of operating leverage (DOL) is a measure of this leverage effect that illustrates how much operating profits fluctuate as sales volume changes. This displays the predicted profit reaction if sales volumes fluctuate. DOL is defined as the percentage change in income (typically expressed as earnings before interest and tax, or EBIT) divided by the percentage change in sales production.

By dividing the change in operating profit by the change in sales revenue, investors can get a ballpark estimate of DOL.

One sector that feels the effects of operating leverage is the airline business. Since the industry is so reliant on consumer demand, the participants’ high fixed expenses are a major factor in the sector’s volatility. Thus, businesses in the airline industry face challenging circumstances as their market share is steadily eaten away by rival firms. When companies’ operating leverage falls below the needed levels, they may be vulnerable to bankruptcy, depending on the state of the market.

Conclusion

Financial and operating leverage are equally important. They both aid firms in increasing profits and decreasing expenses. So, the sticking point is whether or not a business can simultaneously employ both of these levers.

Operating leverage allows a corporation to increase its profits by making more efficient use of its fixed expenses. They can use financial leverage by switching from a 100% equity capital structure to one with a 50% equity, 60% equity, 70% debt, or 90% debt capital structure. A better rate of return may be generated, and taxes could be lowered, even if a shift in the capital structure required the company to make interest payments.

That’s why increasing the company’s rate of return and decreasing its expenses within a specific period can be done with the help of both operating leverage and financial leverage.