Harry Markowitz had a distinguished career in economics for decades before being awarded the Nobel Prize.

Markowitz, who was born on August 24th, 1927 in Chicago, Illinois, was initially drawn to the fields of physics, astronomy, and philosophy, and he became a devoted follower of David Hume’s beliefs in his youth. Throughout his time as a student at the University of Chicago, he pursued his interest in Hume’s ideas. When he was a student at the institution, Markowitz was invited to join the Cowles Commission for Research in Economics.

Markowitz received his Master’s and Doctorate degrees in Economics from the University of Chicago after completing his Bachelor’s degree there. Markowitz studied under such renowned professors as Milton Friedman, Jacob Marschak, and Leonard “Jimmie” Savage during his stay there. Both Markowitz’s article on “Portfolio Selection” and his 1952 RAND Corporation employment were published in the Journal of Finance.

His Modern Portfolio Theory (MPT) is still widely used as a technique for managing investment portfolios and achieving diversified, profitable results.

What is Modern Portfolio Theory?

Investments can be chosen using modern portfolio theory (MPT) to optimise total returns within a predetermined risk budget.

As stated in his 1952 article “Portfolio Selection” for the Journal of Finance, American economist Harry Markowitz was the first to propose this strategy. His contributions to contemporary portfolio theory earned him the Nobel Prize years later. The concept of diversity is central to the MPT framework. These days, most investments are either extremely high-risk or extremely low-reward. Markowitz proposed that investors may maximise their returns by adjusting the proportion of each they invested in based on their own risk preferences.

Modern Portfolio Theory : Where it Came From?

Before Markowitz’s introduction of MPT, the majority of investment strategies were narrowly tailored to a single stock. Investors were accustomed to sifting through the market for investments that would yield satisfactory returns without exposing them to undue risk.

Net present value (NPV) was a tool used by investors to identify these superior equities, and NPV was derived from discounting stocks’ expected cash flows into the future to arrive at their value. Stocks with higher potential for rapid profit growth were heavily weighted in the investment mix.

Markowitz argued that the net present value theory is inadequate since it suggests that picking the “best” portfolio involves picking the stock with the highest predicted NPV. He warned that taking such a stance was inherently dangerous and that, despite widespread agreement among financial experts that portfolio diversification is key, investors lacked a practical means of achieving it.

Markowitz consulted mathematics and statistics to bolster his understanding as he formulated his idea. He argues that statistical techniques like the mean and variance can be used to construct more robust portfolios on the assumption that stock prices fluctuate at random. An investor could think about correlation if they are considering buying two or more similar stocks.

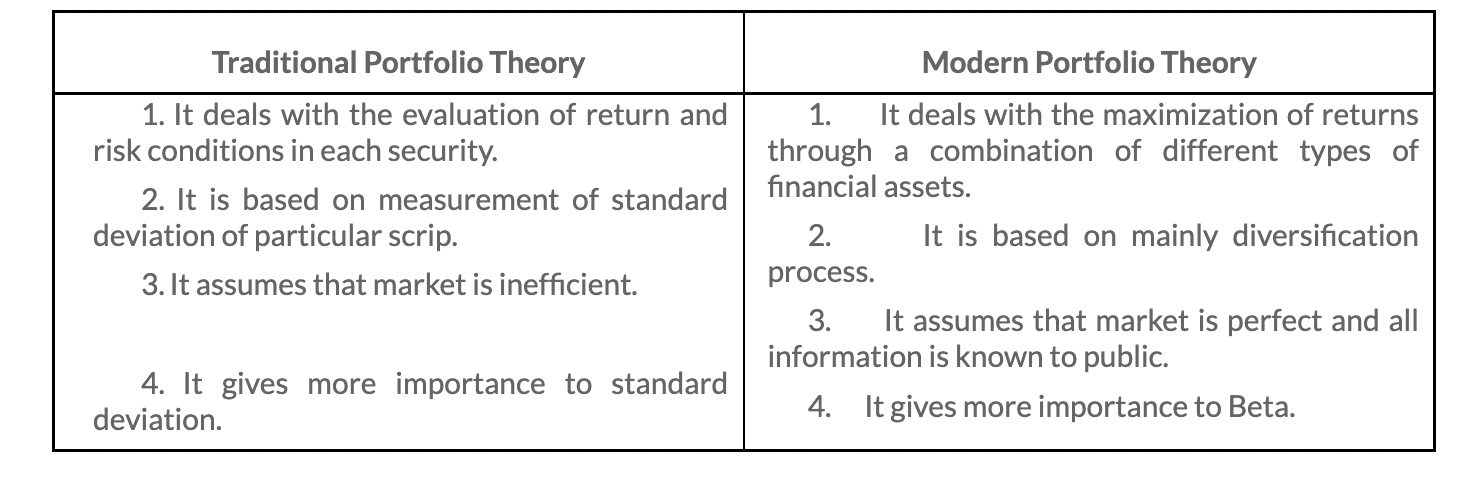

Traditional Portfolio Theory vs. Modern Portfolio Theory

How Does Modern Portfolio Theory Work?

According to the principles of modern portfolio theory, every investor aims to maximise their long-term profits while minimising their exposure to short-term market volatility. When investing, there is a positive correlation between risk and return; therefore, choosing low-risk products like bonds or cash will result in lower returns.

If you want larger profits, you need to invest in riskier assets like equities. However, you might not be willing to take the risk necessary to make those investments. Your level of risk tolerance will determine your answer.

According to MPT, this challenge can be overcome by increasing portfolio diversity. According to this school of thought, it’s best to invest your money in a wide variety of things.

The Modern Portfolio Theory (MPT) states that a portfolio can have a high-risk asset or investment and lower-risk assets or investments simultaneously. If this is the case, its risk will be less than the risk of the underlying assets or investments if taken separately, as the risk of one investment would be offset by the return of another.

You wouldn’t, for instance, put all your money into high-risk equities or low-return bonds. Rather, you would invest in both at the same time and hold them for the longest feasible time to maximise your return.

How to Achieve It?

It’s not wise to choose investments based on which ones expose you to the most danger in the hopes of earning the biggest possible profits.

Markowitz advocated placing the portfolio on the “efficient frontier.” That’s why it’s important to strike a good balance between risk and reward to ensure you maximise your profit with little exposure.

Allocation of Strategic Assets

A passive, or strategic, strategy is the simplest method to build a successful portfolio. In this strategy, investors purchase and maintain a wide range of assets and investments that tend to perform differently from one another. That is to say, they do not exhibit the same degree of volatility in response to changes in the market.

These are a set percentage of the overall portfolio. Examples include the fact that stock market risk is often higher than bond market risk. It’s possible that a portfolio with both stocks and bonds can generate a satisfactory rate of return at a manageable level of risk.

Investments in stocks and bonds have an inverse relationship. It is common knowledge that bond prices decline when stock prices rise. The use of the MPT method helps mitigate the impact of a fall in a single asset class on the value of the portfolio as a whole.

Even if you’re following a deliberate, planned strategy for allocating your assets, you still need to periodically rebalance your holdings. That way, you can make sure your portfolio is well-balanced and in line with your long-term objectives.

Two Fund Theorem

A diversified investment portfolio is not required for MPT compliance. One can, according to the theory, construct a successful portfolio using just two different types of mutual funds. Using this method, you won’t have to select certain stocks.

With this method, you could end up with a portfolio consisting of two funds:

- 50% large-cap, mid-cap, and small-cap stocks

- 50% corporate bonds and short-term, medium-term, and intermediate-term government bondss

Criticisms

Critics of MPT argue that it ignores the real world because all the metrics it employs are based on projected values, or mathematical claims about what is predicted rather than real or existing. Since investors must utilise equations based on projections based on previous measurements of asset returns and volatility, these predictions are susceptible to change due to variables currently not known or considered at the time of the equation.

Due to MPT’s attempts to forecast risk in terms of the potential for losses without a rationale for why such losses could occur, investors are left to estimate based on historical market data. This results in a probabilistic, rather than a structural, analysis of the risk.

To rephrase, the MPT model’s mathematical precision creates the illusion of order when none exists in the real world of investing. For instance, Sanjay Basu, a researcher in the late 1970s, showed that low price-to-earnings ratio (P/E) firms beat high P/E stocks, despite the theory predicting otherwise. Additionally, a separate study conducted in the 1980s by scholar Rolf Banz showed that small-cap equities were superior to large-cap ones.

To sum it up, the following are the drawbacks of MPT:

- Risk, reward, and correlation, which form the basis of MPT, are not based on current data but rather on the past. It’s possible that this information is no longer relevant due to shifts in the market.

- Market-Price Theory (MPT) operates on the basis of a standard set of assumptions about the behaviour of markets. Due to the dynamic nature of the economy, these projections may not pan out.

Conclusion

The Modern Portfolio Theory takes into account the interdependence of a portfolio’s holdings in addition to the risks inherent in each individual holding. It takes advantage of the fact that losses on one asset might be partially offset by losses on a negatively linked asset. It has been observed, for instance, that the price of crude oil is inversely related to the price of airline stocks.

Splitting your investment capital in half between crude oil and airline shares eliminates the risk associated with the unique characteristics of both assets. Airline stocks are expected to rise in value as oil prices fall, offsetting any losses from oil stocks.

Pingback: MarkoVitz Theory - Harry Markowitz Portfolio Th...