THE INEVITABLE WATER CRISIS

Water problems rarely begin with a headline. They build quietly in the background, almost unnoticed, until the system reaches a point where it can no longer cope.

When Cape Town came close to “Day Zero” in 2018, it felt sudden. A global city preparing for taps to run dry. But the reality was very different. The stress had been building for years before it became visible.

That pattern repeats more often than we think. From California facing one of its worst droughts in centuries to Israel turning scarcity into a long-term strategy, the shift is always the same. The problem stays hidden until it reaches a tipping point. And once it does, the response is forced and expensive.

India is not there yet. But it is moving in that direction.

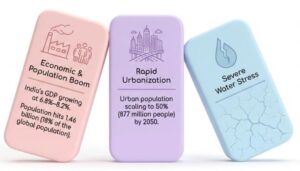

Today, India supports close to 18% of the world’s population with just about 4% of its freshwater resources. Per capita water availability has already fallen to levels that place large parts of the country in the water stressed category. Groundwater, which has quietly supported both cities and agriculture for decades, is being extracted faster than it can replenish.

And yet, it still feels manageable.

Water continues to arrive through tankers. Borewells continue to go deeper. Cities continue to expand. The system stretches just enough to avoid immediate disruption.

That is what makes this phase deceptive.

Because water stress does not show up like other problems. It does not immediately reflect in prices or output. It builds beneath the surface, creating a system that looks stable but is becoming increasingly fragile.

Every country that has faced a severe water crisis has followed a similar path. Years of silent pressure. A gradual tightening of supply. And then a moment where incremental fixes stop working.

India is still in the first phase. But the direction is becoming clearer.

And this is where the story becomes more interesting.

Because unlike most crises, this one does not just destroy value. It quietly begins to create an entire ecosystem around solving it.

INDIA’S GROWING WATER DEFICIT

At the heart of India’s water story is a simple mismatch: demand is rising faster than dependable supply.

India’s total water demand is projected to approach 1,500 BCM by 2030, while available supply is estimated at only 700 to 750 BCM. In practical terms, the country could face a gap large enough to leave nearly half of projected demand unmet.

This is not just a population issue. It is a growth issue.

Urbanisation is increasing household demand for piped and reliable water. Industrialisation is adding higher-value consumption from sectors such as power, chemicals, refining, semiconductors, and green hydrogen. At the same time, agriculture remains the largest consumer and continues to depend heavily on groundwater. In fact, 82% of groundwater is consumed by agriculture, primarily thirst crops like rice and wheat.

The composition of demand is also changing.

Earlier, shortages could sometimes be managed through intermittent supply or local workarounds. That becomes harder when demand comes from cities and industries that require continuous, quality-controlled water. A thermal power plant, refinery, or chip facility cannot operate efficiently on uncertain supply.

Supply, meanwhile, is far less flexible.

Freshwater resources are finite, rainfall remains uneven, storage infrastructure is limited, and groundwater in many regions is already under stress. Unlike power capacity or manufacturing output, water supply cannot be expanded quickly through incremental capex alone.

That is why the emerging deficit matters.

When demand outpaces supply in a persistent way, the response shifts from sourcing more freshwater to using existing water more efficiently through treatment, recycling, leakage reduction, desalination, and reuse.

This is the point where scarcity begins to create an industry.

THE WATER EXISTS; BUT THE QUALITY DOESN’T?

Scarcity is only one side of India’s water challenge. The other, and often less appreciated side, is quality.

A significant share of available water cannot be used productively without treatment. Estimates suggest nearly 70% of India’s surface water is polluted. Rivers, lakes, and local water bodies increasingly carry untreated sewage, industrial discharge, and agricultural runoff.

This changes the supply equation.

Water may exist physically, but if it is unsafe for drinking, unsuitable for industrial processes, or costly to treat, it is not truly available in economic terms.

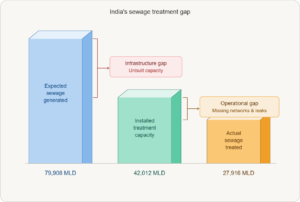

The sewage numbers illustrate the scale of the issue. India generates roughly 62,000 MLD of urban sewage, yet treatment capacity remains well below that level, and actual treated volumes are lower still. Even where installed capacity exists, utilisation gaps persist due to network constraints, under-maintenance, or operational inefficiencies.

The result is a negative cycle.

Untreated wastewater re-enters rivers and groundwater, reducing future usable supply and increasing the cost of purification for cities and industry. In effect, quality deterioration amplifies quantity stress.

This is why water treatment is no longer a secondary service.

It is becoming a core part of the supply chain.

For municipalities, treatment is essential to public health and distribution. For industry, it is necessary for compliance, process reliability, and water security. For investors, this matters because every decline in raw water quality increases the need for filtration, sewage treatment, recycling, and advanced reuse systems.

India’s water problem, therefore, is not only that there is too little water.

It is that too much of the water available now needs to be processed before it can be used.

And this is where the story starts to move from scarcity to solutions.

THE RESOURCE THAT CAN SLOW AN ECONOMY

When water starts constraining growth

Water stress becomes economically important when it begins to affect output, investment, and operating reliability.

India is moving into that phase.

The country is expanding industrial capacity across sectors that are highly water dependent. Power generation alone is expected to add nearly 80 GW of capacity, while refining, chemicals, electronics manufacturing, and emerging segments such as semiconductors and green hydrogen are also scaling up. These industries do not just need water in volume. They need consistent and often high-purity supply.

That distinction matters.

Household shortages create inconvenience. Industrial shortages can create downtime, higher costs, and lost production. For many sectors, unreliable water becomes a direct business risk.

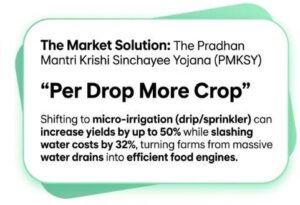

The policy response reflects this shift. India has already committed close to ₹99,500 crore toward water sector initiatives, while the broader investment pipeline across schemes exceeds ₹8 lakh crore. This level of capital allocation suggests water is increasingly being treated as core infrastructure rather than a peripheral utility issue.

Globally, the same pattern is visible. Water-stressed regions in the Middle East have invested heavily in desalination, while Africa is targeting nearly $30 billion annually by 2030 to build water infrastructure.

Most inputs to the economy can be scaled. Energy capacity can be added. Raw materials can be imported. Logistics can be expanded.

Water behaves differently.

When freshwater becomes constrained, the cheapest source of “new water” is often not extraction, but recovery through treatment, reuse, leakage reduction, and process efficiency.

That is why water is no longer only an environmental theme. It is becoming a productivity and competitiveness theme.

For India, this is a critical transition. As the economy formalises and industrialises, growth will increasingly depend not just on access to power, roads, or labour, but on access to reliable water.

The shift from availability to reliability is not just solving a problem.

It is laying the foundation for a long-term infrastructure and technology-driven sector.

HOW POLICY IS BUILDING A NEW INDUSTRY?

Water stress alone does not create an industry. It creates urgency.

An industry forms when urgency is matched with policy, funding, and execution capacity. That is increasingly what is happening in India.

The clearest evidence is the scale of public commitment. India’s water-related investment pipeline is estimated at ₹8 lakh crore+, spanning rural drinking water, urban sewerage, river rejuvenation, groundwater management, and treatment infrastructure. Few utility segments currently have this breadth of policy support.

The flagship example is the Jal Jeevan Mission. Since launch, rural tap water coverage has risen from roughly 17% in 2019 to more than 80%, translating into over 14 crore household connections. Under JJM 2.0, the programme has been extended to 2028 with an expanded outlay of ₹8.69 lakh crore.

The significance of JJM 2.0 is not only scale, but design.

Each major programme is solving a different part of the problem, but together they are building a complete system.

The focus is shifting from asset creation to service delivery through digital monitoring, source sustainability, and local operations and maintenance. In investment terms, this moves the opportunity from one-time EPC contracts toward recurring O&M and lifecycle revenues.

Urban India is seeing a parallel buildout. Programmes such as AMRUT and Namami Gange are accelerating sewage networks and treatment capacity, with targets exceeding 20,000 MLD of additional STP capacity by 2026.

The funding mix is equally important. Roughly 60% is expected from the Centre, 30% from states, with the balance supported by institutions such as the World Bank and ADB. That diversified capital base reduces execution dependence on a single source.

For the private sector, this changes the opportunity set materially.

The first phase rewards contractors that can build quickly. The next phase is likely to reward companies that can operate assets efficiently, reduce non-revenue water, enable reuse, and meet tighter compliance standards.

In short, policy is no longer only responding to scarcity.

It is actively creating demand visibility for the water industry.

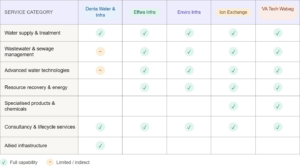

INDUSTRY: WHERE THE REAL WINNERS COULD EMERGE?

By now, the opportunity in the water sector is fairly clear. What is less obvious is how unevenly that opportunity is distributed.

At first glance, most companies in this space appear to be doing similar work. They build treatment plants, lay pipelines, and execute water and wastewater projects. But once you look beneath the surface, the differences in business models, economics, and risk profiles begin to stand out.

And those differences matter far more than the headline growth.

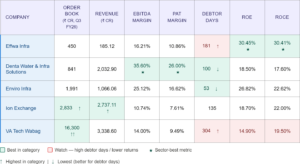

The current upcycle has lifted most players. Order books are healthy across the board, supported by a strong pipeline of government projects. Execution-focused companies have scaled quickly, with revenues crossing ₹900–1,000 crore levels in some cases and margins holding firm in the mid-20s.

On the face of it, this looks like a very efficient outcome. Strong growth, healthy profitability, and improving return ratios.

But this is also where one needs to be careful.

A large part of this performance is linked to the current phase of the capex cycle. As long as project inflows remain strong and execution stays on track, these businesses can deliver attractive growth. The challenge lies in the nature of that growth. It is still largely dependent on fresh order wins, competitive bidding, and timely payments from government bodies.

That makes the model inherently sensitive to both the pace of tendering and the discipline of execution.

A different picture emerges when you move into industrial water and compliance-driven segments.

Here, the dynamics are not entirely dictated by the lowest bid. Instead, reliability, process efficiency, and adherence to environmental norms become critical. This tends to shift the conversation from pure execution to technical capability.

The numbers reflect that shift.

Even at a smaller scale, certain players are delivering return ratios that are meaningfully higher than the broader group. This is not accidental. Industrial clients are less tolerant of failure, and that allows specialised players to command better economics, provided they can execute consistently.

The trade-off, however, is concentration risk. Smaller order books and a narrower client base mean that growth can be sharper, but also more volatile. Working capital pressures also tend to be more pronounced in such models.

At the other end of the spectrum are the more integrated players.

These companies operate across multiple parts of the water cycle. They combine engineering with technology, execution with operations, and in some cases, domestic projects with international exposure.

This diversification shows up clearly in their financial profile.

Margins may not always be the highest in the sector, but revenue visibility tends to be stronger. Order books are often several times annual revenues, providing a longer runway. More importantly, the mix of business includes elements that are less dependent on new project awards, such as operations, maintenance, and recurring service contracts.

That changes the quality of earnings.

It reduces dependence on a single capex cycle and allows for a more stable growth trajectory over time.

One of the more revealing differences across companies is not in reported margins, but in how quickly cash is realised.

Debtor cycles vary widely across the sector. Some companies are able to convert revenue into cash relatively quickly, while others operate with significantly stretched receivable periods.

This is not a trivial distinction.

In project-driven businesses, longer working capital cycles can dilute returns, even when profitability looks strong on paper. It also increases dependence on external funding and exposes companies to delays in payments or project milestones.

Over time, this becomes a key differentiator between businesses that scale efficiently and those that struggle despite growth.

As the sector evolves, these differences are becoming more important.

Execution-led growth is being recognised, but it is also being viewed in the context of its cyclicality. Specialised capabilities are attracting attention because of their pricing power. Integrated models are beginning to be valued for their ability to deliver more stable and diversified earnings.

The first phase rewarded order book growth. The next phase is likely to reward balance sheet strength, cash conversion, recurring O&M revenues, industrial exposure, and technology depth.

That means the opportunity in water is real, but broad sector exposure is not enough. Stock selection and business model quality are likely to matter more than the theme itself.

WHERE THE NEXT PROFIT POOL COULD EMERGE?

The first phase of India’s water cycle was centred on asset creation. Building pipelines, expanding household connectivity, adding treatment plants, and improving access.

That phase is still underway, but the next opportunity may lie less in building new assets and more in improving the economics of assets already created.

The clearest example is sewage treatment. India generates roughly 62,000 MLD of urban sewage, yet effective treatment remains materially lower than generation. Even broader installed capacity estimates of 42,000+ MLD translate into actual treated volumes closer to 28,000 MLD.opportunity

That gap is significant.

It suggests the problem is no longer only shortage of infrastructure. It is also underutilisation, weak network connectivity, maintenance gaps, energy inefficiency, and inconsistent operations.

In practical terms, this has shifted value from EPC contractors toward operations and maintenance providers.

A treatment plant creates one pool of revenue when it is built. It can create another, often more durable pool of revenue when it has to run efficiently for the next 15 to 20 years.

That is why the design of Jal Jeevan Mission 2.0 is notable. The programme’s expanded ₹8.69 lakh crore outlay is accompanied by a shift toward utility-style service delivery, digital monitoring, and local O&M accountability. This indicates policy is beginning to reward performance, not only construction.

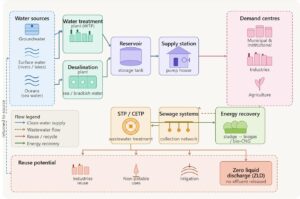

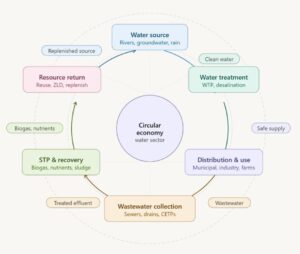

The second emerging profit pool is reuse.

When freshwater becomes constrained, treated wastewater becomes economically valuable. It can be redirected toward thermal power plants, industrial cooling, construction, landscaping, and process use after advanced treatment.

Countries that moved early show what this can become. Israel now reuses over 80% of wastewater, turning scarcity into supply security. India remains far below that level, implying a long runway for growth in recycling infrastructure and advanced treatment technologies.

The third layer is industrial water.

Sectors such as chemicals, pharmaceuticals, steel, semiconductors, refining, and green hydrogen require reliable process water and increasingly face stricter discharge norms. That supports demand for higher-value solutions such as Zero Liquid Discharge, membrane filtration, ultrafiltration, and reverse osmosis systems.

Unlike commoditised municipal EPC, these segments are more technical, less price-driven, and often better for margins.

A fourth, often overlooked opportunity is retrofits.

India has already built a meaningful installed base of water assets over the last decade. Many of these facilities will require automation upgrades, debottlenecking, process optimisation, and energy-efficiency improvements. Historically, these brownfield opportunities can deliver faster execution and attractive returns on capital.

The sector can therefore be viewed in three stages:

Build through new infrastructure creation. Optimise through better utilisation and O&M. Monetise through reuse, industrial supply, and technology-led upgrades.

The first stage creates revenue growth. The later stages often create better earnings quality.

That may be where the next phase of value creation in the water sector comes from.

WHY WATER COULD BE THE NEXT LONG-DURATION THEME?

India’s water sector is moving beyond a narrow infrastructure theme into a broader long-duration industrym opportunity.

The drivers are now visible and mutually reinforcing. Demand is rising, supply is constrained, water quality is deteriorating in several regions, regulation is tightening, and policy capital is already committed at scale. Few sectors benefit from this many structural tailwinds simultaneously.

The demand-supply imbalance remains the foundation of the story. India’s water demand is projected to approach 1,500 BCM by 2030, against available supply of only 700 to 750 BCM . At the same time, nearly 70% of surface water is estimated to be polluted, which means headline availability overstates usable supply.

That is why estimates for India’s water and wastewater market point to 1.6x to 1.7x growth over the coming years.

That combination creates a persistent need for treatment, recycling, storage, and distribution efficiency.

The policy response is already large enough to matter financially. India’s broader water investment pipeline exceeds ₹8 lakh crore, while Jal Jeevan Mission 2.0 alone carries an outlay of ₹8.69 lakh crore with an increasing focus on service delivery, monitoring, and long-term sustainability. In parallel, programmes such as AMRUT, Namami Gange, and groundwater initiatives continue to expand treatment and network capacity.

This matters because the sector’s revenue pools are broadening.

The first phase was driven by EPC opportunities such as pipelines, treatment plants, and connectivity. The next phase is likely to include recurring O&M contracts, digital monitoring, leakage reduction, industrial reuse, retrofit projects, and advanced treatment systems.

That progression usually improves earnings quality.

There is also a sizeable installed-base opportunity. India generates around 62,000 MLD of urban sewage, while installed treatment capacity of 42,000+ MLD results in actual treatment closer to 28,000 MLD. This gap suggests the next decade will not only be about new assets, but also about making existing assets productive.

For listed companies, this means outcomes will diverge.

Execution-led businesses may continue benefiting from tender pipelines, but will remain exposed to bidding intensity and working capital cycles. Industrial specialists may benefit from higher-margin compliance-led demand. Integrated platforms with technology, O&M capability, and diversified end markets may be best placed if the sector shifts toward lifecycle contracts and recurring revenues.

That distinction is important. The opportunity is real, but it is not uniform.

From an investor’s perspective, water now resembles other sectors at the early stage of formalisation: strong macro demand, rising policy support, fragmented competition, and evolving business models. In such phases, the first gains often come from growth. Longer-term value tends to accrue to companies with capital discipline, execution credibility, and durable revenue streams.

Water may never be the most visible sector in the market.

But sectors built on necessity rather than sentiment often compound quietly.

India’s water industry appears to be entering that phase now. Broad optimism will not be enough.

The winners are unlikely to be those merely present in the sector.

They are more likely to be those best positioned for what the sector becomes next.

If you need guidance on how to start your stock market journey, how much capital is enough to begin with, how to do smart investing, or how to take informed stock market decisions, you can join Strategic Alpha’s ‘The Conviction Club’. This is a membership program, especially curated to help investors become aware and knowledgeable about stock market trends, news, and technical aspects, so that they can become their own experts.

Our YouTube channel, weekly webinars, and digital resources available on the website can help you learn the basics of the stock market. For regular updates on trends, one-to-one sessions with experts, and detailed learning modules, you can join the Conviction Club, which is the online community of like-minded investors sharing knowledge and thoughts to grow together.

Subscribe to the Strategic Alpha Newsletter now to get the latest updates about weekly webinars.

Join Me On My Telegram Channel Where I Share Much More Value Adding Knowledge Of Investing/ Trading: Click Here

Also, Don’t Forget To Follow Us On Our Social Media Accounts:

Facebook: https://www.facebook.com/strategicalpha/

Instagram: https://www.instagram.com/strategicalpha/

Twitter: https://twitter.com/suyog_dhavan

YouTube: https://bit.ly/2IIqztO

Disclaimer: Strategic Alpha and Suyog Dhavan are not SEBI-registered investment advisor. The content provided is purely for educational purposes and should not be construed as financial or investment advice. Viewers are encouraged to conduct their own research or consult with a SEBI-registered professional before making any investment decisions.