Have you ever come across a company whose business remained largely stagnant for nearly a decade yet quietly holds the ingredients of a potential turnaround?

In a firm where revenues barely moved, the market lost interest, and the stock stayed under the radar, but beneath the surface, the foundations of the business have slowly been changing.

What if the real story isn’t the past decade of stagnation but the strategic transformation unfolding over the last few years?

Is it a shift in strategy, a better product mix, or industry dynamics finally turning favorable?

Opportunities often lie in identifying these early green shoots of change before they fully reflect in the numbers.

This brings us to Orient Bell Limited, a company with nearly five decades of experience in manufacturing and trading ceramic and vitrified tiles.

Over the past few years, the company has been undergoing a structural shift in its business model, with EBITDA margins expanding by around 2% to 6%+ levels and the potential to double margins over the next few years if the strategy plays out as planned.

So what exactly is changing? To understand this, we first need to look at how the Indian tile industry itself is evolving and where Orient Bell fits into this changing landscape.

The Indian Ceramic Tiles Industry

The Indian ceramic tiles industry is one of the largest in the world and plays an important role in the global tiles market. India is currently the second-largest producer, consumer, and exporter of ceramic tiles after China, accounting for roughly 11–15% of global production and about 10.9% of global consumption.

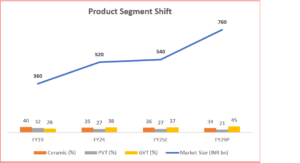

The domestic tile market has grown steadily over the past decade. The market size expanded from ₹360 billion in FY19 to around ₹531 billion in FY25, reflecting a 6.7% annual growth rate. However, growth slowed in the last two years, with the industry expanding only around 3% in FY24 and FY25.

Despite this slowdown, the long-term outlook remains strong. The industry is expected to reach nearly USD 15.8 billion by 2030, growing at an estimated 8.2% CAGR.

India is projected to produce more than 2 billion square meters of tiles annually, making it one of the largest manufacturing hubs globally.

India’s per capita tile consumption currently stands at around 0.8 square meters, which is significantly lower than the global average of 1.4 square meters and far behind major tile-consuming markets such as Brazil (3.4 sqm), China (4.0 sqm), and Vietnam (4.4 sqm).

As urbanization, housing demand, and renovation activity increase, India’s per capita consumption is expected to rise to around 1 square meter by FY29, representing nearly a 25% increase from current levels.

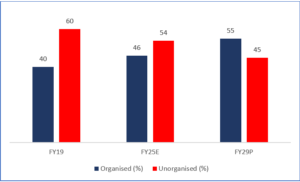

However, the industry remains highly fragmented. Nearly 70% of manufacturers operate in the unorganized sector, which keeps pricing highly competitive and limits margin expansion for many players.

Product Evolution: The Shift Toward Premium Tiles

One of the most important structural shifts in the industry is the change in product mix.

Tiles are broadly divided into three categories:

- Ceramic tiles

- Polished vitrified tiles (PVT)

- Glazed vitrified tiles (GVT)

In FY19, ceramic tiles dominated the market with 40% share, while PVT held 32% and GVT accounted for 28%.

But the mix is changing rapidly.

By FY29, the share of GVT is expected to rise to around 45%, while ceramic tiles could decline to 34%, and PVT may fall to 21%.

The growth data clearly shows this shift.

Glazed vitrified tiles demonstrate the strongest growth trajectory across all time periods, growing at:

- 12.0% CAGR (FY19–FY24)

- 4.2% (FY24–FY25)

- 16.4% projected growth (FY25–FY29)

In comparison:

- Ceramic tiles grew 6.4%, 1.4%, and 7.0% during the same periods.

- Polished vitrified tiles (PVT) grew 4.2%, 2.7%, and 3.0%

This makes GVT the fastest-growing and most premium segment in the industry.

Housing Trends Are Also Driving Premium Tiles

Changes in the housing market are also influencing tile demand.

Historically, a large share of tile consumption came from mid-income housing projects priced between ₹60 and ₹75 lakh. However, this segment has slowed significantly in the past two years, with supply and sales declining 14–35%.

Developers are increasingly shifting toward premium housing projects priced above ₹1 crore, where margins are higher.

At the same time, luxury housing demand is rising strongly, driven by higher disposable incomes and changing consumer preferences.

The luxury housing market is expected to grow at around 21.8% CAGR, potentially reaching $18.3 billion by 2030.

Because luxury homes typically use larger, premium vitrified tiles, this trend further strengthens demand for GVT and large-format tiles.

Industry Capex Reflects This Premium Shift

This structural shift is also visible in where companies are investing their capital.

Most new investments in the tile industry are focused on:

- Large slab manufacturing

- Porcelain and vitrified tiles

- Premium surfaces like quartz and marble

Very little new capacity is being added in basic ceramic tiles, clearly indicating industry premiumization.

Even listed players are following this trend.

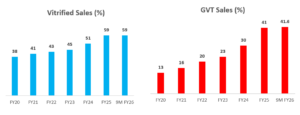

For example, Orient Bell increased the share of vitrified tiles in its portfolio from 38% in FY20 to around 59% in 9M FY26. Within this, GVT sales increased sharply from 13% to around 41.6%.

Housing Trends Are Also Driving Premium Tiles

Changes in the housing market are also influencing tile demand.

Historically, a large share of tile consumption came from mid-income housing projects priced between ₹60 and ₹75 lakh. However, this segment has slowed significantly in the past two years, with supply and sales declining 14–35%.

Developers are increasingly shifting toward premium housing projects priced above ₹1 crore, where margins are higher.

At the same time, luxury housing demand is rising strongly, driven by higher disposable incomes and changing consumer preferences.

The luxury housing market is expected to grow at around 21.8% CAGR, potentially reaching $18.3 billion by 2030.

Because luxury homes typically use larger, premium vitrified tiles, this trend further strengthens demand for GVT and large-format tiles.

Industry Capex Reflects This Premium Shift

This structural shift is also visible in where companies are investing their capital.

Most new investments in the tile industry are focused on:

- Large slab manufacturing

- Porcelain and vitrified tiles

- Premium surfaces like quartz and marble

Very little new capacity is being added in basic ceramic tiles, clearly indicating industry premiumization.

Even listed players are following this trend.

For example, Orient Bell increased the share of vitrified tiles in its portfolio from 38% in FY20 to around 59% in 9M FY26. Within this, GVT sales increased sharply from 13% to around 41.6%.

Peers are also shifting in the same direction.

At Somany Ceramics, the tile mix now stands at:

· Ceramic tiles – 33%

· PVT – 26%

· GVT – 41%

Notably, GVT share increased by 7% YoY from FY24, highlighting how rapidly companies are moving toward premium tiles.

Morbi: The Ceramic Capital of India

No discussion about the Indian tiles industry is complete without understanding Morbi, the country’s ceramic manufacturing hub.

Located in Gujarat, Morbi accounts for 80–90% of India’s ceramic tile production and hosts over 900 manufacturing units.

The cluster produces nearly 4 million square meters of tiles every day. The industry generates roughly ₹60,000 crore in annual revenue. In 2025, Morbi aims to double its ceramic output by 2027 and reach a turnover of ₹80,000 crore, employs around 400,000 people, and accounts for nearly 95% of India’s ceramic production. It’s expected that this year it will grow 6% in exports.

Morbi’s success comes from its low-cost manufacturing ecosystem, which allows it to produce tiles up to 30% cheaper than China while still being closer in perceived quality to premium Italian ceramics.

This combination of low cost and acceptable quality helped Morbi dominate export markets across the United States, Africa, the Middle East, and Europe.

Market Structure: Organized vs. Unorganized

The Indian tiles industry is divided between organized branded players and unorganized manufacturers, primarily concentrated in Morbi, Gujarat.

Organized players currently account for roughly 46% of the market, and this share is expected to increase to around 55% by FY29 as branding, distribution strength, and product innovation become more important.

Among the listed companies:

- Kajaria Ceramics leads with ~17% organized market share

- Somany Ceramics and Prism Johnson hold around 9% each

- Asian Granito has ~6% share

- Orient Bell holds around 5% share

The remaining market is largely controlled by hundreds of small manufacturers from Morbi.

Current Headwinds in the Industry

Despite its scale, the ceramic industry is currently facing several structural challenges.

First, China enjoys a strong technological and scale advantage. Chinese ceramic companies operate large integrated factories, invest heavily in R&D, and receive strong government policy and financing support, allowing them to innovate faster and produce at lower costs. In contrast, most Morbi factories are small or mid-sized family-owned units, which lack the scale, technology, and financial backing to compete effectively.

China is also expanding globally by setting up manufacturing plants in regions like Nepal, Africa, and Gulf countries. These factories often operate as local companies on paper but are effectively Chinese-backed operations. From these locations, Chinese firms supply tiles into markets that were historically dominated by Indian exporters, sometimes even dumping products into nearby markets such as North India.

At the same time, export restrictions and anti-dumping duties in several countries have reduced India’s export competitiveness. As export demand weakens, Morbi manufacturers are increasingly pushing their production into the domestic market, creating oversupply and intense price competition. Because many Morbi factories are small and operate on thin margins, prolonged price pressure has already forced several units into financial stress, NPA situations, and even factory closures.

Housing Slowdown in the US and Europe

Indian tile exports to the United States have increased dramatically over the past decade.

- 2013: ~344,000 sq ft exports

- 2023: ~40.5 million sq ft exports

For context, the US currently accounts for about 9% of Indian tile exports.

However, both the US and European housing markets are currently weak.

United States

In 2024, US home sales fell to about 4 million homes, the lowest level since 1995.

Home prices have risen significantly. Over the last 10 years, US house prices almost doubled.

Over the past five years, median home prices in the US have increased around 50%, further weakening affordability.

Many Americans bought houses during 2020–2022 when interest rates were very low (3–4%).

Now if they sell their house and buy another one, they would have to take a new loan at 6–7%.

So they prefer staying in the same house instead of moving.

This reduces home sales, renovations, and housing transactions. This reduces housing turnover and renovation demand.

Signs Housing Sales Are Slowly Improving

Toward the end of 2025, home sales started improving slightly.

Example:

- Existing home sales increased 5.1% in December

- New home sales also improved earlier.

Mortgage rates also fell slightly, which helped demand a bit.

But housing affordability is still a problem, as right now mortgage rates are above 6%, which makes buying houses expensive, + builders are still building new houses. This means more homes are coming into the market.

The housing affordability index is still 35% worse than before COVID.

Europe

Europe is facing a similar problem. Over 300 units in Morbi are exported to various European countries.

Housing loan demand in 2023 declined 30% YoY. House prices in the EU have increased by up to 60% on average since 2015, with some member states seeing rises of over 200%. At the same time, household incomes have not kept pace, leaving many Europeans struggling to cover their housing expenses.

Today, housing consumes nearly one-fifth of the average EU household’s income. In major cities, affordability pressures are even more severe, with many residents spending over 40% of their income on housing, limiting property transactions and slowing housing activity across the region.

Domestic Oversupply and Pricing Pressure

As exports decline, a large portion of Morbi’s production is now redirected to the domestic market, which has created significant oversupply.

To clear inventory and maintain cash flow, many manufacturers are selling tiles at extremely thin margins or sometimes even below cost.

This aggressive pricing has caused average selling prices across the industry to decline sharply and offering further discounts, creating pressure on both unorganized and organized players.

In addition to this, in anticipation of demand from 2023 onwards, public listed players like Kajaria Ceramics, Somany Ceramics, and Orient Bell increased their capacity so much; as a result, they are still waiting for the demand to come back.

Dealers have responded by keeping very low inventory levels, as prices have been continuously falling and the number of tile designs and sizes available has increased significantly. This makes stocking decisions difficult and further slows the demand cycle.

Energy Costs and the Middle East Crisis

Another major challenge for the ceramic industry is energy cost, particularly natural gas and propane used to run tile kilns.

In India, natural gas is taxed under VAT rather than GST, which means manufacturers cannot claim input tax credit. This makes fuel costs significantly higher compared to many competing countries.

Geopolitical tensions in the Middle East, particularly the Iran–US–Israel conflict, have disrupted global energy supply chains, increasing uncertainty for energy-intensive industries like ceramics. Since nearly 40% of India’s crude imports pass through the Strait of Hormuz, any disruption directly affects fuel availability.

Recently, Gujarat Gas Ltd. cut industrial gas supply by about 50% due to tight LNG availability, leaving many Morbi ceramic factories with only a few days of propane and about a week of natural gas reserves, raising risks of production disruptions and higher costs.

Understanding the Business

Orient Bell Limited currently operates three company-owned manufacturing plants and works with two associated manufacturing partners, taking the company’s total production capacity to over 42.4 million square meters annually as of March 2025.

Product development has been a major focus area for the company. In FY25 alone, Orient Bell launched:

- 266 new SKUs in Glazed Vitrified Tiles (GVT)

- 455 new SKUs in the ceramic segment

With these additions, the company now offers a portfolio of over 4,000 SKUs, catering to a wide range of consumer preferences and price points from mass-market tiles to premium décor products.

A large product portfolio is important in the tiles industry because it helps dealers and showrooms attract more customers and offer better design choices.

What Changed at Orient Bell in the Last Four Years?

The ceramic tile industry is currently going through premiumization, consolidation pressure, and intense price competition from the Morbi cluster. In such an environment, companies that can build strong distribution networks, improve product mix, and strengthen brand positioning are more likely to emerge stronger.

Interestingly, Orient Bell spent the last few years quietly working on exactly these areas.

Before understanding the investment thesis, it is important to first understand how the company operates and what changes management has implemented over the past four years.

The Core Problem: Distribution Weakness

Despite having a long operating history, Orient Bell faced several structural issues in its business model until a few years ago.

The most significant problem was distribution strength.

Weak Presence in Key Markets

Management acknowledged that the company had limited distribution in South and West India, two of the most important tile consumption markets in the country.

This meant:

- fewer dealers

- limited showroom visibility

- lower brand awareness.

As a result, the company remained over-dependent on North Indian markets.

Product Mix Was Not Ideal for Retail

Another structural challenge was the product mix.

Earlier, nearly 65–70% of Orient Bell’s volumes came from ceramic tiles.

The problem with ceramic tiles is that they are:

- lower value products

- highly commoditized

- dominated by low-cost Morbi manufacturers.

Because of this, even when Orient Bell had dealers, those dealers often preferred selling cheaper Morbi tiles, which were easier to move in the market.

Underdeveloped Retail Channel

The company also relied heavily on institutional and project sales, such as builder orders and large projects. And the builders generally ask for a 10-15% discount, which further erodes the margin.

However, in the tiles industry, retail distribution is the real brand builder.

Companies like Kajaria Ceramics built their leadership by creating large dealer networks and strong retail showrooms across India.

Orient Bell’s retail presence was relatively underdeveloped.

The Strategic Shift

Around 2021–2022, the management realized that competing effectively required a stronger retail ecosystem and a better product mix.

This triggered a major strategic shift in distribution and branding.

Over the next few years, the company implemented several important changes.

Expanding the Dealer Network

The first step was to significantly expand the dealer network.

Today Orient Bell has:

- 2000+ business partners

- 3000+ dealers across India

The company is particularly focusing on Tier-2 and Tier-3 cities, where housing development and renovation demand remain strong.

Management commentary suggests that Tier-3 cities now contribute nearly 59% of sales, while Tier-1 accounts for around 23% and Tier-2 around 18%, highlighting how fast the company is expanding in smaller cities.

Building Retail Experience Stores

Another major initiative was the creation of OBTX – Orient Bell Tile Boutiques.

These are specialized experience showrooms designed to showcase premium tile designs.

Today the company operates 300+ tile boutiques across India, which together contribute roughly 42% of total sales, and is focusing on renovating it for better customer experience.

These stores help the company:

- display premium products

- influence retail buyers

- strengthen brand visibility.

Strengthening Sales in South and West India

Management also began actively expanding its sales teams and distribution networks in South and West India along with focusing on increasing the brand awareness in regions where the company historically had weak penetration. Management clearly stated that in Q3 FY26 they are going to penetrate deep into southern markets by strengthening their distribution.

By strengthening dealer relationships and building stronger local sales teams, Orient Bell is gradually improving its presence in these high-consumption markets.

Using Technology to Support Dealers

The company has also introduced several digital tools to support dealers and improve customer experience.

These include:

- AI-based tile visualization tools

- Digital tile design simulators

These tools allow customers to visualize how tiles would look in their homes before making a purchase, helping dealers close sales more effectively.

Product Strategy: Moving Toward Premium Tiles

Distribution expansion alone was not enough. The company also had to upgrade its product mix.

Earlier, the business was heavily skewed toward ceramic tiles, but management gradually shifted focus toward vitrified and glazed vitrified tiles (GVT).

Orient Bell increased the share of vitrified tiles in its portfolio from 38% in FY20 to around 61% in 9MFY26. Within this, GVT sales increased sharply from 13% to around 44%.

Premium tiles typically offer:

- better dealer margins

- higher realizations

- stronger retail demand.

To support this shift, the company added the Dora GVT production line, which has an annual capacity of 3.3 million square meters. Orient Bells are even focusing on larger size tiles to cater to the growing demand.

Due to the entry-level GVT tiles getting commoditized, the management is focusing on increasing their production towards the premium GVT segment.

This investment has helped Orient Bell expand its presence in premium vitrified tiles, particularly in South and West markets.

Potential Triggers

1. Operating Leverage from Capacity Utilization

Currently, Orient Bell operates at around 65% capacity utilization. As demand improves and utilization moves toward 90–100% levels, the company can significantly increase output without major additional fixed costs.

This creates operating leverage, where revenue growth translates into disproportionately higher profitability. With existing capacity, the company estimates it can generate ₹1,000–1,200 crore in revenue, almost double the current sales, along with expansion in the margins once utilization reaches optimal levels.

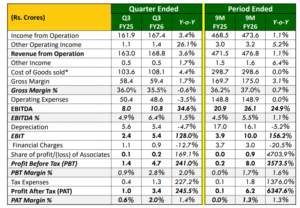

With COP lower by 4.5% y-o-y, they are able to expand margins by 2% in the last 2 yrs and EBITDA margin up 150 bps vs. Q3 last year and 110 bps vs. 9M last year by operating at 60% capacity and with the help of an increase in volume without an increase in the price of the product. So we can just have a rough estimate in our mind that when the capacity utilization reaches 90-100% levels, what level of margin expansion can happen with an increase in volume along with an increase in prices of products and product mix change.

2. Product Mix Shift Toward Higher-Margin Tiles

Another key driver of margin expansion is the increasing share of Glazed Vitrified Tiles (GVT) in the company’s portfolio.

GVT tiles command better pricing, higher dealer margins, and stronger retail demand compared to ceramic tiles. As Orient Bell continues to expand its GVT offerings, launch new SKUs, and push premium products through its retail network, the overall product mix is expected to improve.

This shift alone has the potential to significantly expand EBITDA margins over the coming years.

3. Retail and Branding Strategy

The company is increasingly focusing on brand building, retail visibility, and dealer engagement.

Through initiatives like Tile Boutiques, digital visualization tools, and expanded distribution networks, Orient Bell is positioning itself more strongly in the retail market.

Retail-led sales tend to offer higher margins, better pricing power, and stronger brand recall, which can gradually improve the company’s overall profitability.

Continued marketing investment strengthening brand visibility and trust, leading to a positive impact on conversion rates

4. Capex Cycle Largely Complete

A large portion of the company’s capacity expansion and modernization capex was completed around 2023, at 234 crores.

Management has indicated that no major capex is expected in the next three years, which means incremental revenue growth will not be accompanied by significant increases in depreciation or fixed costs.

This allows the company to benefit fully from operating leverage as demand grows.

5. Potential Industry Tailwinds from Export Recovery

Exports from the Morbi ceramic cluster are expected to increase by around 6% this year.

If export demand strengthens, some of the excess supply currently present in the domestic market could gradually reduce.

Lower domestic oversupply + no new capacity addition expected to be added further in the next 6-8 months could help stabilize or even improve average selling prices (ASP) for tiles, which would benefit manufacturers across the industry, including Orient Bell.

6. Industry Consolidation

The prolonged price pressure and cost challenges have already forced many small ceramic manufacturers in Morbi to shut down or face financial distress.

Since a large portion of Morbi consists of small and mid-sized factories operating on thin margins, sustained industry stress could lead to further consolidation.

Over time, this could reduce excess capacity and allow organized players with stronger brands and distribution networks to gain market share.

Conclusion

Over the past four years, Orient Bell Limited has focused on fixing structural weaknesses in its business by strengthening distribution, expanding its dealer network, and building retail presence through Tile Boutiques. The company also shifted its product mix from commoditized ceramic tiles toward higher-margin vitrified and GVT tiles. With most of the capex cycle completed, the company now has sufficient capacity to scale revenue without significant additional investment. If demand improves and capacity utilization rises, Orient Bell could benefit from operating leverage and better margins. Additionally, potential industry consolidation and export recovery from the Morbi cluster may reduce pricing pressure and support profitability. Overall, the company has spent the last few years building the foundation for future growth.

At Strategic Alpha, we keep coming up with such detailed analysis of companies to help investors make informed decisions. Whether you are a beginner or an experienced investor, we can help make your investing journey smoother and better. Join our weekly webinars to learn basics of stock market investing or become a member of our ‘Conviction Club’ to receive regular updates, connect one-to-one with our mentors, and grow with like-minded investors.

If you need guidance on how to start your stock market journey, how much capital is enough to begin with, how to do smart investing, or how to take informed stock market decisions, you can join Strategic Alpha’s ‘The Conviction Club’. This is a membership program, especially curated to help investors become aware and knowledgeable about stock market trends, news, and technical aspects, so that they can become their own experts.

Our YouTube channel, weekly webinars, and digital resources available on the website can help you learn the basics of the stock market. For regular updates on trends, one-to-one sessions with experts, and detailed learning modules, you can join the Conviction Club, which is the online community of like-minded investors sharing knowledge and thoughts to grow together.

Subscribe to the Strategic Alpha Newsletter now to get the latest updates about weekly webinars.

Join Me On My Telegram Channel Where I Share Much More Value Adding Knowledge Of Investing/ Trading: Click Here

Also, Don’t Forget To Follow Us On Our Social Media Accounts:

Facebook: https://www.facebook.com/strategicalpha/

Instagram: https://www.instagram.com/strategicalpha/

Twitter: https://twitter.com/suyog_dhavan

YouTube: https://bit.ly/2IIqztO

Disclaimer: Strategic Alpha and Suyog Dhavan are not SEBI-registered investment advisor. The content provided is purely for educational purposes and should not be construed as financial or investment advice. Viewers are encouraged to conduct their own research or consult with a SEBI-registered professional before making any investment decisions.