What if I told you that nearly one-third of India’s housing value is concentrated in just one region and most investors are still underestimating it?

What if the same market is witnessing a silent but powerful shift:

- Premium and upper mid-income housing steadily capturing a larger share of demand

- And millionaire households in MMR in its core city rising ~194% since 2021, fundamentally altering buying power

And yet the biggest question remains unanswered:

Is this a cyclical boom or a structural shift that could define the next decade of wealth creation?

Because when developers like Lodha openly state that nearly 50% of their future presales will come from premium and upper mid-income segments, and players like Ajmera are doubling down on large-scale luxury developments in Mumbai this is no longer just confidence in the market.

It is capital allocation backed by conviction.

And if that’s true then the real question isn’t “Is Mumbai real estate attractive?”

Can a relatively new entrant like Raymond Realty, just six years into the market, position itself to capture this shift and emerge as a meaningful proxy for Mumbai’s evolving real estate cycle?

The Power Centre: Why MMR Is Not Just Leading It Is Dominating

To understand the opportunity, one must first understand the scale of Mumbai Metropolitan Region (MMR). Maharashtra also tops state-level rankings: it accounts for roughly 35–40% of RERA-registered projects nationwide, reflecting its dominant role in India’s real-estate sector.

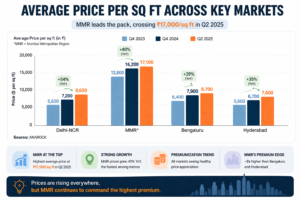

MMR today is not just another large real estate market; it is India’s most dominant housing engine. Estimates suggest that it contributes roughly 31–33% of housing sales value across the top seven cities, while Mumbai city alone accounts for nearly 29% of total residential transactions by value. This level of concentration is rare. It indicates that any structural shift in Mumbai is not local it has national implications.

In Mumbai, new supply and sales are concentrated in specific zones. In Q1 2026, the Western and Eastern Suburbs together accounted for 45% of all new residential launches. This is a direct response to both ongoing infrastructure upgrades like the Coastal Road and Metro corridors, and the affordability gradient compared to the island city.

Transaction data from these suburbs shows a clear preference for mid-segment housing (48% of new supply), but with a significant 27% share for high-end and luxury projects. This dual demand structure makes these corridors resilient. For instance, a standard 1 BHK in a well-connected suburb like Kandivali can range from ₹60 lakh to ₹1.5 crore.

But what makes MMR so powerful is not just demand it is the quality of demand.

Three structural forces are driving this:

1. Economic Gravity and High-Income Job Creation

Mumbai continues to attract high-income employment through financial services, global capability centres, and corporate headquarters. This creates a buyer base that is:

- Less sensitive to interest rates

- More focused on asset quality

- Willing to pay for lifestyle and location

2. Infrastructure Is Expanding the City Without Expanding Distance

Perhaps the most underestimated driver of Mumbai real estate is infrastructure.

Projects like:

- Mumbai Trans Harbour Link (reducing travel time by ~45%)

- Navi Mumbai International Airport (expected 2026)

- Metro corridors transforming east-west connectivity

- Coastal Road improving South Mumbai access

are not just improving commute they are compressing geography.

Locations that were once considered peripheral are now entering the investment mainstream.

Take Palava, for instance. It is transitioning from a distant suburb into a planned urban node, supported by connectivity upgrades and future-ready infrastructure. Similarly, Wadala is emerging as a potential third CBD, attracting developer interest and large-scale capital commitments.

This explains why developers are not just launching projects they are doubling down on micro-markets.

3. Micro-Markets Are Becoming the Real Investment Battleground

MMR is no longer a single market it is a network of micro-economies.

- Western Suburbs are driven by metro connectivity and rental demand, making them stable investment zones

- Thane is emerging as a high-growth affordability-driven market with improving infrastructure

- Navi Mumbai is positioning itself as an infrastructure-led appreciation story, backed by the airport and MTHL

This layered structure allows Mumbai to cater to multiple income segments simultaneously, making it more resilient than other cities.

The Data Is Already Signalling a Shift

Recent transaction trends confirm that the market is not slowing it is evolving.

Mumbai recorded 15,516 property registrations in March 2026, the highest for the month in over a decade. But the more important insight lies beneath the surface:

- The ₹1–2 crore segment increased its share from 32% to 38%

- The sub-₹1 crore segment declined from 46% to 39%

This is not a marginal shift. It is a clear movement of demand toward higher ticket sizes.

Even within unit sizes:

- The 500–1,000 sq ft category is gaining share

- Ultra-small units are losing traction

Affordable vs Premium

The Numbers Tell the Story First

The divergence between affordable and premium housing is no longer anecdotal it is sharply visible in the data.

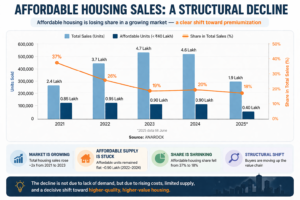

Affordable housing, which once formed the backbone of India’s residential market, has been steadily losing relevance:

- Its share has declined from 38% in 2019 to ~18% in 2025

- Homes priced below ₹50 lakh recorded a ~17% YoY decline in sales

- Homes priced between Rs 50 lakh and Rs 1 crore saw an 8% YoY decline in sales, shrinking the combined share of affordable and mid-income housing in total transactions.

- New launches in the segment fell even more sharply, by 28%, indicating weakening developer interest

Even the broader mass segment is showing stress, with homes priced between ₹50 lakh and ₹1 crore witnessing an 8% YoY decline, highlighting that pressure is not limited to the lowest ticket sizes but extends into the mid-income category as well.

Why Affordable Housing Is Struggling

- Affordability has structurally weakened

Price-to-income ratios have stretched to 8–12x in metros, making EMIs unaffordable for first-time buyers. - Interest rates hit this segment the hardest

Even small rate hikes reduce loan eligibility significantly, pushing entry-level buyers out of the market. - Developers are exiting due to low margins

High land and construction costs make affordable housing financially unattractive for developers. - Mismatch between product and buyer expectations

Buyers now prefer better amenities and connectivity, while affordable housing often lacks both. - Policy support has limited real impact

Price caps and subsidies have not kept pace with urban realities, especially in cities like Mumbai.

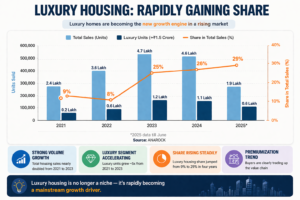

At the same time, the premium and ultra-premium end of the market is expanding with equal force:

- Luxury housing demand (₹4 crore and above) has grown ~28% YoY across seven major cities

- The ₹4–6 crore segment alone with sales of 7,000 homes has seen an extraordinary ~85% surge in demand in H1 FY25, reflecting strong absorption at higher price points according to a joint report by CBRE South Asia and Assocham.

- Within premium categories, the ₹3–5 crore segment has grown ~14%, while ultra-luxury (>₹5 crore) continues growing by 8%.

What makes this shift even more compelling is its alignment with wealth creation trends. India is witnessing a sharp rise in wealth, with the number of millionaire households expected to grow by 90% to 871,700 by 2025, according to the Mercedes-Benz Hurun India Wealth Report 2025. Mumbai alone houses over 1.42 lakh millionaire households of the total 1,78,600 millionaire households in Maharashtra, forming a deep and expanding demand base for premium real estate. The number has surged 194% since 2021, reflecting both the strength of the state’s economy and the scale of Mumbai’s financial ecosystem.

At the same time, income growth for the broader population is far more measured. Maharashtra’s per capita income, growing at roughly 9% annually, is only marginally ahead of housing price inflation in prime Mumbai markets, where prices are rising at ~5–7% per year. On paper, this looks balanced. In reality, it creates a widening divide.

Why Premium Housing Is Expanding

- Rapid wealth creation is driving demand

A ~194% rise in millionaire households since 2021 has created a strong buyer base for high-value homes.

- Buyers are upgrading, not just buying

Buyers are no longer evaluating homes purely on price demand, post covid demand has shifted toward larger homes, better amenities like gyms, pools, co-working spaces and lifestyle-driven living.

- Lower sensitivity to interest rates

Premium buyers are less dependent on financing, making demand more resilient. - Developers are prioritizing high-margin segments

Capital is being allocated to premium projects where profitability and cash flows are stronger. - Supply discipline is supporting price growth

Controlled launches and falling inventory are creating a healthier demand-supply balance.

Raymond Realty

Every real estate company claims to build homes. Very few set out to rebuild the way homes are delivered.

As the Raymond Group nears its centennial celebration in 2025, the demerger of its realty business into Raymond Realty Ltd. marks more than just a corporate restructuring it reflects the emergence of a focused, standalone platform built for scale. What makes this transition even more compelling is the fact that this journey began just six years ago in 2019, making Raymond Realty one of the youngest yet fastest-scaling players in Mumbai’s highly competitive real estate market.

When Raymond Realty entered the market in 2019, it wasn’t stepping into an empty space it was entering one of the most fragmented, execution-challenged industries in India. Delays were common, quality was inconsistent, and customer experience was often an afterthought.

And that is precisely where the company chose to position itself.

As management puts it, the ambition from day one was not to chase scale blindly, but to solve three fundamental gaps in the industry delivering quality products, ensuring timely (or even early) delivery which is evident from its 101% sales CAGR over the last 4 years with good collections and bookings yoy, and creating a customer-first experience in a market that has historically been developer-centric.

This may sound simple on paper, but in real estate, it is exceptionally difficult to execute. Regulatory complexities, approval delays, and capital constraints often force developers to optimize for margins rather than customers.

Raymond Realty chose to take the opposite approach.

The company consciously prioritised customer experience even if it meant short-term trade-offs on margins, with the belief that over time, this would create a brand premium and allow it to gain market share irrespective of broader market cycles.

Execution as a Moat

What truly differentiates Raymond Realty is not just intent it is execution speed.

One of the most critical bottlenecks in real estate is the time taken from:

Signing a project → Launching it for sales

- Industry average: 3–5 years

- Raymond Realty: 18–24 months

This is not a marginal advantage.It is a structural moat.

Faster time-to-market leads to:

- Quicker monetization of projects

- Better capital efficiency

- Lower execution risk

- Higher internal rate of return (IRR)

In a business where delays destroy value, speed becomes a competitive advantage that compounds over time.

What the Business Looks Like Today

Six years into its journey, Raymond Realty has moved from intent to meaningful scale.

Today, the company operates with a portfolio visibility of ~₹40,000 crore GDV, out of which:

- ~₹10,500 crore worth of projects have already been launched

At the core of this portfolio lies its Thane land bank, which acts as both a growth engine and a cash generator.

- Total land bank: ~100 acres (Thane)

- Under development:

- 40 acres (~4 mn sq ft)

- Revenue potential: ~₹9,000 crore

- Future development:

- 60 acres (~7 mn sq ft)

- Revenue potential: ~₹16,000 crore

- Total Thane potential:

- ~₹25,000 crore GDV

This provides long-term visibility, with monetization expected over the next 7 years.

Expanding Beyond Thane: Enter the JDA Strategy

While Thane provides stability, Raymond Realty’s next phase of growth is being built through a strategic shift toward Joint Development Agreements (JDAs).

The company has already signed six JDAs across Mumbai’s prime micro-markets, including:

- Bandra

- Mahim

- Sion

- Wadala

These projects together represent a ~₹14,000 crore GDV opportunity with monetization expected over the next 5 years.

What is JDA And Why It Matters

A Joint Development Agreement (JDA) is a partnership model where:

- The landowner contributes land

- The developer builds, markets, and sells the project

- Revenues (or profits) are shared

Instead of deploying large capital to acquire land, the developer uses execution capability as leverage.

To expand beyond Thane, the group has also operationalised its JDA-led growth strategy through Ten X Realty Limited (TRL), a step-down wholly owned subsidiary focused on joint development projects across MMR and Navi Mumbai.

In FY25, TRL reported a sharp scale-up with gross revenue of ₹560.7 crore and a profit after tax of ₹18.1 crore, compared to negligible revenue and losses in the previous year. This reflects early success in executing the asset-light expansion model. Notably, TRL operates as an integral part of Raymond Realty’s broader platform, driving its Mumbai-centric growth strategy.

Why JDA Is Central to Raymond’s Future

This shift is not tactical it is strategic.

By adopting a JDA-led model, Raymond Realty is aiming to:

- Scale faster without heavy balance sheet stress

- Maintain disciplined capital allocation

- Focus on high-IRR opportunities (20–25% target)

- Expand into premium micro-markets within MMR

The company is already exploring further JDA opportunities and even looking to extend this model into Pune, indicating that this approach will drive future growth beyond Mumbai.

Where Raymond Realty Stands Today

If you connect the dots, a clear picture emerges:

- A company built on customer-first philosophy

- Backed by a strong parent brand (Raymond Group)

- Operating in India’s most valuable real estate market (MMR)

- With:

- ₹40,000 crore GDV pipeline

- A mix of owned land (Thane) and asset-light JDAs (Mumbai)

- A structural advantage in execution speed

Raymond Realty: 9M FY26 Performance

If the macro story explains why Mumbai real estate is shifting, the last nine months of Raymond Realty explain how a company positions itself within that shift.

The first half of FY26 needs to be understood correctly because misreading it leads to the wrong conclusion. At first glance, performance looked underwhelming:

- Q2 bookings stood at ₹455 crore

- Growth appeared muted despite strong industry tailwinds

But the reality was very different.

The company entered FY26 with extremely low available inventory, especially in its core market:

- Thane: ~91% inventory already sold out

- Bandra: ~50% inventory sold

This meant that sales were not constrained by demand they were constrained by lack of product to sell.

Because at the same time:

- Collections remained strong at ₹409 crore in Q2

- Market demand across MMR continued to remain stable

The Real Build-Up: Laying the Foundation for H2

While sales looked soft, the company was actively preparing for a much larger scale-up.

Instead of chasing short-term numbers, Raymond Realty focused on pipeline creation and capital deployment discipline:

- Launch pipeline expanded from an initial 3–4 projects to 7 projects for FY26

- Total development visibility increased to ~₹40,000 crore GDV

- Core markets sharpened around Thane, Bandra, Wadala, Sion, and Mahim

At the same time, the company doubled down on its asset-light strategy, with a strong push toward JDAs:

- JDA pipeline: ~₹14,000 crore GDV

- Raymond share: ~₹11,500 crore

- Execution horizon: 5 years

This was not incremental growth.

This was business model transformation in motion.

Q3 FY26: The Inflection Quarter

By Q3, the pieces started falling into place.

With launches kicking in, performance saw a sharp acceleration:

- Bookings surged to ₹743 crore (+47% YoY)

- 9M FY26 bookings reached ₹1,504 crore

- Revenue grew +56% YoY to ₹766 crore

This confirmed a very important cycle:

Inventory → Launch → Sales conversion

Launch Engine Now in Motion

The company’s launch strategy, which was only a plan in Q1, became execution reality in Q3:

- Total planned launches for FY26: ~7 projects

- Q3:

- 2 JDA projects launched

- Q4 pipeline:

- Sion, Wadala, Mahim, Thane expansions

Portfolio expansion is now visible:

- Current: ~9 projects

- Post Q4: ~13 projects

JDA Strategy The Big Structural Shift

The most important transformation happening within Raymond Realty is not visible in quarterly numbers it is visible in its business mix.

- JDA contribution:

- ~22% (FY25) → Targeting ~50% by FY28

- Total JDA pipeline:

- 6 projects (~₹14,000 crore potential)

Breakdown:

- 2 launched (already contributing)

- 2 launching in Q4

- 2 lined up over next 12–15 months

This shift is critical because it allows the company to:

- Scale without heavy land acquisition

- Maintain 20–25% IRR discipline

- Improve capital efficiency

In simple terms Raymond is transitioning from a land owner → capital allocator.

Margins: Why They Look Weak Today And Why That Matters

One of the biggest misconceptions around the company right now is its margin profile.

At first glance, margins appear lower than expectations. But there is a hidden catch

Reason 1: Demerger Impact

Earlier, Raymond Realty operated as a division within Raymond Ltd., where several costs were not fully allocated.

Now, post demerger:

- All common costs are fully absorbed

- Reported margins appear lower, but are more realistic

Reason 2: JDA Accounting Distortion

This is where most investors get it wrong.

Under accounting standards:

- Rehab portion (given to landowners) is booked as revenue

- But it carries only ~5% margin

Whereas: Actual project margins are ~18–20%

As a result early-stage projects show lower blended margins & as more projects get added up, margins gradually expand and will stop fluctuating in a larger range.

Reason 3: Early-Stage Project Economics

- Launch phase = higher costs (marketing, approvals)

- Pricing follows a “hockey stick curve”

- Lower at launch

- Higher as project matures along with increase in price of property each year.

Pricing Trends across various micro-markets

Across core micro-markets:

- Thane: ~6–7% growth

- Bandra: ~5% growth

- Wadala/Sion: ~5–7% stable trend

Inventory & Cash Flow Dynamics

Understanding Raymond Realty also requires understanding its cash cycle.

- Pre-launch phase:

- High outflows (approvals, setup)

- Post-launch:

- Strong inflows (customer collections)

This creates a natural cycle:

0–18 months: muted cash flow → followed by strong inflows

With launches now accelerating, the company is entering the cash-generating phase.

Capital Allocation

The company has remained clear on its capital strategy:

- Annual Business Developement addition:

- ₹6,000–10,000 crore GDV

- Return threshold:

- 20–25% IRR

Priority:

- Execute existing pipeline

- Add high-quality JDAs

- No aggressive land buying

- Focus on capital-light growth

Core Thesis

Execution-Led Differentiation

Raymond Realty has demonstrated relatively strong execution capabilities, with project turnaround timelines of 18–24 months compared to the broader industry range of 3–5 years. This allows for faster monetization cycles, improved capital efficiency, and relatively lower execution risk.

Valuation and Margin Trajectory

The company is currently trading at ~12–13x P/E, while operating at ~12% EBITDA margins, which are at the lower end of its historical range. Management has indicated a margin trajectory towards ~20%, with further improvement possible (~25%) driven by scale benefits and product mix. This indicates potential for margin normalization over the medium term.

Pre-Sales Momentum and Growth Visibility

Raymond Realty has reported pre-sales of ₹3,023 crore for FY26 (+31% YoY), supported by a strong Q4 performance of ₹1,519 crore (+139% YoY). This reflects healthy demand trends and traction in recent project launches.

Operating Performance Trends

The company has maintained financial discipline, with ~46% CAGR in collections over the last five years. While collections declined ~8.6% YoY (partly due to seasonality such as monsoon impact in H1), pre-sales growth (~50% CAGR) indicates alignment between execution and demand trends.

Wadala: Strategic Exposure to Emerging Micro-Market

Raymond Realty’s ~₹5,000 crore Wadala project, developed under a JDA-led asset-light model, is located in a micro-market benefiting from ongoing infrastructure developments such as MTHL, Metro connectivity, and the Eastern Freeway, along with the emergence of BKC 2 as a business hub. JDA projects, including Wadala, typically command higher realizations (1.5x–2x vs. Thane), reflecting location and product positioning differences.

Project Pipeline Visibility

With the addition of a ₹3,000 crore GDV project in Kandivali, the total pipeline has expanded to ~₹43,000 crore GDV. This provides visibility on future launches and execution across the Mumbai Metropolitan Region (MMR).

Earnings Profile and Outlook

Based on a steady quarterly profit assumption of ~₹60 crore, the annualized profit run-rate is estimated at ₹200+ crore (~₹30 EPS). This provides a reference point for evaluating the company’s earnings trajectory in the context of its ongoing project pipeline and margin progression.

Embedded Land Bank Value Not Reflected in Market Cap

Raymond Ltd monetized a 20-acre Thane land parcel in 2019 for ₹700 crore, implying ~₹35 crore per acre. The company still holds ~100 acres in the same micro-market, indicating substantial embedded value. Even conservative benchmarking suggests a land value running into several thousand crores. This underlying value is not fully captured in the current market capitalization.

If you need guidance on how to start your stock market journey, how much capital is enough to begin with, how to do smart investing, or how to take informed stock market decisions, you can join Strategic Alpha’s ‘The Conviction Club’. This is a membership program, especially curated to help investors become aware and knowledgeable about stock market trends, news, and technical aspects, so that they can become their own experts.

Our YouTube channel, weekly webinars, and digital resources available on the website can help you learn the basics of the stock market. For regular updates on trends, one-to-one sessions with experts, and detailed learning modules, you can join the Conviction Club, which is the online community of like-minded investors sharing knowledge and thoughts to grow together.

Subscribe to the Strategic Alpha Newsletter now to get the latest updates about weekly webinars.

Join Me On My Telegram Channel Where I Share Much More Value Adding Knowledge Of Investing/ Trading: Click Here

Also, Don’t Forget To Follow Us On Our Social Media Accounts:

Facebook: https://www.facebook.com/strategicalpha/

Instagram: https://www.instagram.com/strategicalpha/

Twitter: https://twitter.com/suyog_dhavan

YouTube: https://bit.ly/2IIqztO

Disclaimer: Strategic Alpha and Suyog Dhavan are not SEBI-registered investment advisor. The content provided is purely for educational purposes and should not be construed as financial or investment advice. Viewers are encouraged to conduct their own research or consult with a SEBI-registered professional before making any investment decisions.