For a company that has seen years of subdued growth, the latest quarter from Bajaj Consumer Care Ltd. stands out.

In Q3 FY26, consolidated profit after tax rose 83% year-on-year to ₹46.37 crore. Revenue from operations grew over 30% to ₹306.09 crore. These are not incremental improvements. They mark a clear shift in momentum.

The market responded immediately. The stock hit the 20% upper circuit following the results, reflecting renewed interest after a prolonged period of limited movement.

But the real question is not about the stock reaction.

After years of revenue stagnation, has the underlying business finally begun to move or is this just a strong quarter in isolation?

THE STORY SO FAR

The Bajaj Group was born out of India’s freedom struggle. It traces its roots back to 1953, when the Bajaj Group began marketing hair oils and beauty products under Bajaj Sevashram. Over the decades, the company built a strong presence in the hair oil category and today stands as one of the leading players in India.

At the centre of this story is Bajaj Almond Drops Hair Oil (ADHO), the company’s flagship brand and the market leader in the Light Hair Oil category, with over 60% market share. It is a premium-positioned product and remains the backbone of the business. The brand has scale with over 43 lakh outlets reached in India and a presence in more than 30 countries.

On paper, this is a company with heritage, reach, and a proven track record in its core category.

But there is a flip side.

Over time, the business became heavily dependent on Almond Drops. Nearly 80% of revenues still come from ADHO. That concentration created a structural limitation. Growth avenues were restricted. Any slowdown in the core category directly affected the overall business.

The post-COVID environment exposed this vulnerability more clearly. Rising input costs, inflation, shifts in consumer spending, and muted rural demand created pressure. Revenues remained largely flat for several years. Margins declined. Demand recovery was slower than expected.

The company wasn’t collapsing, but it wasn’t expanding either.

Over the years, the company did introduce new products and attempted to broaden its portfolio. However, these additions had only a marginal impact on the overall revenue trajectory. The business continued to generate largely flat revenues, indicating that the newer initiatives were not yet meaningful growth drivers.

In a rapidly evolving FMCG environment where brands need to keep scaling and aligning with current consumption trends, the question began to surface: had BCCL lost visibility beyond its flagship product?

This was the weak spot.

The challenge, therefore, wasn’t survival. It was reinvention. That’s the backdrop against which the recent numbers need to be viewed.

WHAT HAS CHANGED: SHARPER EXECUTION AND A CLEARER FOCUS

A visible improvement in performance often follows a change in execution discipline. In BCCL’s case, the appointment of Mr. Naveen Pandey as Managing Director from July, 2025, marked an important shift in approach.

Mr. Pandey brings experience from companies such as Marico, PepsiCo, Asian Paints and Unibic; businesses known for scaling brands and strengthening distribution. Since his appointment, the emphasis appears to have moved toward tightening the core business before expanding further.

Reinvigorating the core:

The immediate focus has been on restoring momentum in Almond Drops Hair Oil (ADHO), which continues to contribute nearly 80% of revenues.

Several actions have been visible over the past few quarters –

- Price corrections were implemented in Q1 and Q2 FY26.

- Advertising spends increased 37% year-on-year in Q3 FY26.

- A higher share of advertising is now digital (around 40%).

- Distribution quality and direct reach are being strengthened.

- Greater attention is being given to affordable packs to protect consumer demand.

The impact is measurable.

In Q3 FY26 –

- Revenue grew 30% year-on-year.

- EBITDA margins improved to 18% from 11% in Q3 FY25.

- The quarter saw double-digit volume growth in ADHO, following value-led growth in Q2.

What stands out is that margins expanded despite higher spending. That suggests the improvement was not driven by cost cuts alone, but by a combination of pricing, mix and operating leverage.

Distribution expansion and demand trends:

Distribution expansion is also underway through “Project Aarohan,” which aims to increase direct retail coverage. The company has already expanded reach in FY26, with Phase 2 progressing.

Demand trends are also showing improvement. Urban demand has remained steady, while rural demand, which had been softer post-COVID, has begun to recover over recent quarters. Given the category’s rural exposure, this matters.

The company is also seeing traction in larger pack sizes, which typically support better realisations.

Portfolio discipline:

Beyond ADHO, the approach appears more selective.

Earlier portfolio additions had limited impact on overall revenue, as growth remained flat.

The recent acquisition of Vishal Personal Care Ltd., parent company of Banjara’s brand, suggests a more focused expansion into adjacent categories (entry into natural and ayurvedic personal care segment) rather than broad experimentation.

Importantly, recent growth has been volume-led, especially in the ADHO segment. After price-led value growth in Q2 FY26, Q3 saw double-digit volume growth in the flagship brand. That shift matters. Volume-led growth suggests underlying demand strength rather than just pricing support, and indicates that the brand is gaining traction with consumers.

At the same time, attention within the portfolio is being prioritised, with coconut oil remaining a key category outside ADHO.

The improvement in Q3 FY26 provides early evidence that these changes are beginning to reflect in both growth and margins.

ADHO – THE CORE ENGINE

Almond Drops Hair Oil (ADHO) continues to be the backbone of Bajaj Consumer Care.

It remains the No.1 brand in the Light Hair Oil category with a 63% market share in FY25. The brand has strong distribution reach, with rural penetration across 1.4 million outlets in UP and MP alone, and contributes meaningfully through e-commerce (9% contribution).

During FY25, the company undertook a structured revitalisation of ADHO. This included –

- A new thematic TV campaign focused on hair fall reduction

- 8,000+ TV spots across major Hindi and regional channels

- 18% Share of Voice in Hindi-speaking markets

- 1.7 crore digital reach and 3.9 crore video views

On-ground activations such as Kumbh Mela and Chitrakoot Mela helped strengthen rural engagement, while influencer and digital-led campaigns deepened urban recall.

The strategy around ADHO has clearly been to defend and strengthen the flagship brand through higher visibility, sharper messaging and improved product experience (including packaging changes like flip-top caps).

ADHO remains the primary profit driver of the company.

NON-ADHO – BUILDING THE SECOND LEG

Outside ADHO, the portfolio is broader but still developing in scale.

Coconut Oil:

Bajaj 100% Pure Coconut Oil emerged as a key focus category in FY25. The brand executed a 360° campaign delivering 1,287 GRPs on television, along with 3.05 crore digital views and 82% video-through rates.

The company also introduced multiple channel-specific SKUs, including larger jars for general trade, e-commerce packs and pharmacy-exclusive variants; indicating a more targeted approach to distribution and pack strategy.

Amla Portfolio:

The Amla oil portfolio saw innovation-led growth. Bajaj Sarson Amla became one of the faster-growing variants in North India, supported by changes in fragrance, colour and texture based on consumer feedback.

Ethnic Range:

The Ethnic Range (Henna and Gulab Jal) gained traction, with Bajaj 100% Pure Henna expanding distribution from 1,200 to 4,800+ outlets in modern trade.

Almond Drops Extensions:

The company has also expanded the Almond Drops franchise into shampoo, conditioner, soap and body lotion.

The Ultra-Light Body Lotion launch was supported by digital campaigns achieving 46 lakhs reach and 50 lakh views in Phase 1 alone.

Acquisition – Vishal Personal Care Ltd.:

In FY25, Bajaj acquired VPCL (owner of Banjara’s), a natural personal care brand with –

- ₹50+ crore annual revenue

- 14% four-year CAGR

- 70,000+ outlet reach across five South Indian states

- High single-digit EBITDA

- Debt-free operations

This marks a deliberate expansion into the Ayurvedic and herbal segment.

OPPORTUNITY & RISK

The recent momentum is visible, but sustaining it will require consistency.

On the opportunity side, ADHO has returned to volume-led growth, supported by higher advertising intensity and price corrections taken earlier in the year. EBITDA margins improved from 11% to 18% year-on-year, and MD Naveen Pandey has indicated a medium-term aspiration of moving toward 20–21%, closer to sector levels.

Distribution expansion under Project Aarohan is another structural lever. The company has already added 24,000+ outlets and entered 1,300 new towns, with plans to continue expanding direct reach by roughly 8–10% annually. Rural demand is also showing signs of recovery, which is critical for the hair oil category.

Beyond ADHO, the portfolio is widening gradually. E-commerce grew 29% in FY25, coconut oil is gaining traction across channels, and the acquisition of VPCL adds a foothold in the natural personal care segment and strengthens South India presence.

The company is also working on its international business (contributes around 5% of revenues), which has been weak over last couple of quarters.

However, risks remain.

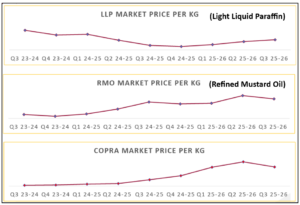

Nearly 80% of revenues still come from ADHO, leaving the business concentrated. Input cost volatility can pressure margins. Execution of Project Aarohan and integration of Banjara’s will need discipline. Competition in hair oils and personal care remains intense. Cost of raw materials, though favourable at the moment, may be affected by geopolitical challenges and other macroeconomic issues.

The direction has improved. The key test now is whether growth in volumes, margins and distribution can hold over multiple quarters.

That will determine whether this is a structural shift or simply a strong phase within a cyclical recovery.

CONCLUSION

For years, Bajaj Consumer Care Ltd. was stable but not expanding. Revenues were flat, margins were under pressure, and growth leaned heavily on one brand.

However, that pattern now appears to be shifting.

The company announced a buyback of up to 57.41 lakh shares (4.02% of equity) at ₹290 per share, aggregating up to ₹166.49 crore. At the same time, it continues to hold over ₹300+ crore in cash on the balance sheet. That combination — improving operating performance and returning capital — signals management confidence in cash flows.

More importantly, this is not a business standing still. As we had discussed in our YouTube video on BCCL over a year ago, the company has been innovating and investing in product development. Those investments are now beginning to show through and could fruition further in the coming quarters as distribution deepens and newer SKUs scale.

Peers in the hair oil and personal care space are also seeing recovery, which suggests the demand environment is improving. But BCCL’s move stands out because of the margin shift.

If margins continue to move closer to sector averages, the impact on EPS could be meaningful; and in consumer businesses, sustained earnings expansion is what drives re-rating.

It is still early. But this time, the improvement looks operational, not accidental. And that makes the difference.

At Strategic Alpha, we keep a track of companies where the real business improvement is just starting, like what we’re seeing here, so that investors can act at the right time. Because when business fundamentals become strong, great long-term opportunities are created. Stay tuned for such relevant updates or become a member of our fastest-growing investors’ community – The Conviction Club!

If you need guidance on how to start your stock market journey, how much capital is enough to begin with, how to do smart investing, or how to take informed stock market decisions, you can join Strategic Alpha’s ‘The Conviction Club’. This is a membership program, especially curated to help investors become aware and knowledgeable about stock market trends, news, and technical aspects, so that they can become their own experts.

Our YouTube channel, weekly webinars, and digital resources available on the website can help you learn the basics of the stock market. For regular updates on trends, one-to-one sessions with experts, and detailed learning modules, you can join the Conviction Club, which is the online community of like-minded investors sharing knowledge and thoughts to grow together.

Subscribe to the Strategic Alpha Newsletter now to get the latest updates about weekly webinars.

Join Me On My Telegram Channel Where I Share Much More Value Adding Knowledge Of Investing/ Trading: Click Here

Also, Don’t Forget To Follow Us On Our Social Media Accounts:

Facebook: https://www.facebook.com/strategicalpha/

Instagram: https://www.instagram.com/strategicalpha/

Twitter: https://twitter.com/suyog_dhavan

YouTube: https://bit.ly/2IIqztO

Disclaimer: Strategic Alpha and Suyog Dhavan are not SEBI-registered investment advisor. The content provided is purely for educational purposes and should not be construed as financial or investment advice. Viewers are encouraged to conduct their own research or consult with a SEBI-registered professional before making any investment decisions.