Summary

At Strategic Alpha, our methodology centers on identifying contrarian opportunities within out-of-favor sectors burdened by temporary headwinds or market overhangs. We view these neglected pockets of the market as fertile hunting grounds for identifying future winners.

Currently, the broader infrastructure space exemplifies this theme. The sector has undergone a two-year consolidation phase following the onset of the 2024 general elections, facing both budgetary constraints and execution headwinds. However, we maintain that infrastructure remains a robust decadal theme, and this recent lull presents a strategic window of opportunity in this sector.

Within the broader infrastructure landscape, the hydropower segment presents a particularly compelling opportunity. The hydropower industry has notably been deprioritized for the last 7-8 years with almost no growth in the installed hydropower capacity. We expect this trajectory to reverse. Hydropower, alongside Pumped Storage Projects (PSP), is poised to become an indispensable pillar of India’s energy security. Furthermore, with China aggressively weaponizing water rights via super-dams near the Indian border, reviving the northeastern hydropower capacity is no longer merely an economic goal; it has become a strategic geopolitical imperative.

Against this backdrop, Patel Engineering emerges as a strong case study for our Fundamental, Technical, Value, Trigger (FTVT) framework, driven by the following factors:

- It is one of the few specialized hydropower EPCs in a moderately concentrated industry with limited competition.

- Strong execution track record of delivering complex projects in the challenging terrains of the Himalayan region.

- It is the only listed pure-play hydropower EPC company (with over 60% of its order book concentrated in hydropower and PSPs).

- It trades at a deeply discounted valuation (~10x P/E and ~0.6x P/B).

- Low leverage (debt to equity ratio of ~0.3x)

Infrastructure Sector: On the Cusp of a Major Breakout Following a Two-Year Consolidation

Over the last few weeks, we have consistently highlighted the infrastructure sector’s structural prospects during our weekly community connect. Specifically, we have been tracking the emergence of a highly bullish technical setup across the broader sector.

Source: Tradingview (Figure: 1)

The broader sector underwent a prolonged structural consolidation and deleveraging cycle between 2008 and 2020. After remaining deeply out of favor for over a decade, it reignited during the 2023-2024 period, driven by a massive surge in government capital expenditure.

Following an aggressive cycle of order awarding, key infrastructure sub-sectors experienced a temporary lull due to the following structural and cyclical headwinds:

- Cost and time overruns for various schemes leading to slow ordering activity.

- Diversion of funds toward welfare schemes.

- Disruption caused by both general and key state elections.

- Execution disruptions caused by the prolonged 2025 monsoon.

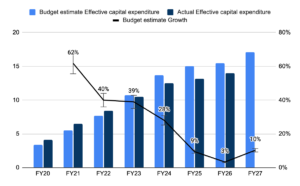

Looking ahead, infrastructure spending is poised for a robust rebound, underpinned by the government’s unwavering focus on capital asset creation. Early green shoots are already emerging, evidenced by the Government of India raising its effective capital expenditure allocation to ₹17.1 lakh crore (an approximate 10% increase) in the FY27 Union Budget.

Source: Government of India Budget documents. (Figure: 2)

While numerous sub-segments stand to benefit from this renewed capex cycle, the energy infrastructure space, specifically grid resilience and stability, has emerged as an urgent national priority.

Grid Stability and Resilience: A Core Priority for the Government

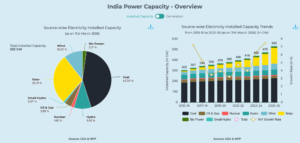

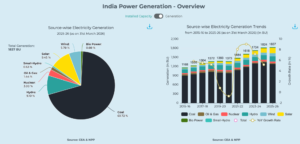

In recent years, India has aggressively pivoted its energy generation mix toward renewables, with solar power attracting the lion’s share of investments. (See Figure 3 for the rapid ramp-up in solar adoption).

Source: CEA (Figure: 3)

Source: CEA (Figure: 4)

However, this rapid scaling of solar capacity, which now accounts for ~10% of India’s overall power generation, has introduced severe intermittency issues. Because solar generation peaks at midday and collapses by evening, it creates a steep mismatch with peak demand hours. Compounded by unpredictable weather patterns, this volatility severely threatens grid stability.

According to a joint CRISIL-FICCI report, pushing the solar energy mix to 20% risks creating a highly unstable grid, while scaling it to 30% would render the grid systemically vulnerable to widespread disruptions.

While this dynamic is currently fueling a capex cycle in distribution transformers, upgrading transmission infrastructure is merely a stop-gap measure. To ensure long-term resilience, India must deploy robust energy storage capacity to absorb short-term power fluctuations and facilitate medium-term peak demand shaving.

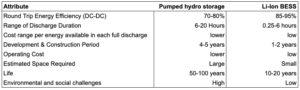

Currently, there are only two commercially viable alternatives at scale for energy storage: Battery Energy Storage Systems (BESS) and PSP.

Source: Niti Aayog, and other public sources for the latest data. (Figure: 5)

We are bullish on both energy storage solutions, viewing them as complementary technologies. Lithium-ion BESS is highly economical for managing intra-day energy fluctuations and addressing short-burst power deficits/surpluses. Meanwhile, pumped hydro storage can be used for much longer power deficit/surplus cycles.

Because Patel Engineering does not operate within the BESS space, the remainder of this report will focus exclusively on the macro opportunity in PSP and traditional hydroelectric power (HEP).

Pumped storage projects: A Solution for Grid Stability.

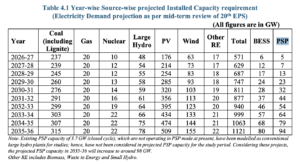

Recently, the Central Electricity Authority (CEA) published its Long-Term National Resource Adequacy Plan for FY27–FY37. In this report, the CEA highlights the surge in power consumption and the continued scaling of solar PV capacity. To balance this volatile solar generation, the report emphasizes the critical role of Energy Storage Systems (ESS), specifically BESS and PHS.

While both technologies are vital, the scale of the projected expansion for PSP is particularly staggering. According to the CEA’s estimates, PSP capacity is slated to grow to 94 GW by FY36, representing a massive leap from the current capacity of ~7.4 GW.

Source: CEA (Figure: 6)

To meet this ambitious target, a robust pipeline is already taking shape. The government has mapped out a pipeline of ~60 GW of PSP capacity to be commissioned by FY32. The execution of this pipeline is already underway; the CEA reports that 10 projects (representing 21.1 GW) are currently under construction, while another 22 projects (totaling ~34 GW) have entered various stages of state clearance and implementation. (Refer to Figure 7 for more details.)

Source: CEA (Figure: 7)

Re-prioritization of Hydropower in India’s Energy Mix

India is home to a vast network of seasonal and perennial river basins that sustain its population of over 1.4 billion. Beyond supporting ecological survival, these river systems, particularly the perennial networks, serve as a major source of clean energy. As of today, India has ~47.7 GW of hydropower capacity, which contributes ~10% to the national energy mix.

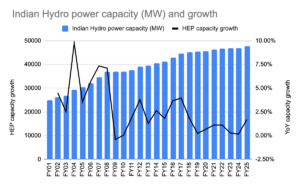

Historically, the capacity growth for hydropower plants has been steadily declining. Figure 8 illustrates a sharp decline in capacity growth from FY18 to FY25, during which capacity grew at an average pace of 0.75% as compared to FY11-FY18 and FY01-FY11 when the growth rate averaged 5.78% and 2.05%, respectively.

Source: CEA (Figure: 8)

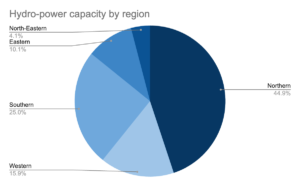

While the historical slowdown might suggest that India’s hydropower capacity has peaked, the reality is quite the opposite. According to the CEA, India’s total hydropower potential is estimated at ~145 GW, of which a mere 32% has been tapped. The remaining unexploited potential lies primarily in the challenging Himalayan terrain and the geopolitically sensitive regions of Jammu & Kashmir and the North-East.

India’s hydropower potential is concentrated in the following regions:

- Brahmaputra Basin: ~65 GW (81% in Arunachal Pradesh alone: ~52 GW)

- Indus Basin: ~34 GW

- Ganga Basin: ~21 GW

- Southern Rivers: ~24 GW

Despite possessing the highest generation potential, the Brahmaputra Basin remains largely unutilized due to a complex mix of economic viability concerns, socio-environmental challenges, poor connectivity, and regional geopolitical risks.

Source: CEA (Figure: 9)

We believe the hydropower industry is poised for significant capacity additions, with a substantial portion of this capacity expected to originate from the North-Eastern region, driven by two key sets of catalysts:

Category 1: Policy, Grid-Stability & Operational Catalysts

Regulatory Reclassification: The recognition of large-scale hydropower plants (25 MW+) as “renewable energy sources” in 2019 has unlocked access to low-cost green financing and concessionary development capital.

Grid Balancing & Intermittency Management: Hydropower facilitates crucial peak-shaving capabilities. It acts as a perfect counter-cyclical complement to solar energy, particularly during the monsoon season when solar generation plummets and river runoffs peak.

Infrastructure Connectivity: Ongoing heavy government investment in North-Eastern road connectivity, tunneling, and heavy transport networks has finally made the execution of complex Himalayan engineering projects logistically viable.

Category 2: Geopolitical & Strategic Imperatives

Countering China’s Upstream Threat: China is currently constructing a massive 60 GW super-dam just 30 km north of the Indian border on the Yarlung Tsangpo (Brahmaputra). This poses two critical strategic risks for India:

- Water Weaponization: Beijing could arbitrarily restrict upstream water flow during dry seasons (potentially reducing flow by up to 85%) or release excess water to trigger artificial flash floods during periods of conflict.

- First-Use Water Rights: Under international water law, the state that first puts a shared river’s waters to beneficial use establishes a stronger legal claim of “prior use” in future water-sharing negotiations.

Shift in Downstream Dynamics: Recent geopolitical shifts in Bangladesh have prompted New Delhi to adopt a more assertive approach to upstream water control, paving the way for expedited domestic hydroelectric project construction.

The Indus Waters Treaty in Abeyance: Following India’s decision to place the active treaty on hold over regional security concerns, New Delhi has a strategic opening to fast-track long-delayed run-of-the-river and storage-based projects on the Chenab and Jhelum river systems in J&K.

According to the CEA’s report titled Master Plan for Evacuation of Power from Hydroelectric Plants in the Brahmaputra Basin, the government intends to evacuate up to ~65 GW of power through high-voltage direct current (HVDC) transmission lines by 2047. This massive undertaking will be executed in phases: targeting 19.5 GW of capacity by 2035, followed by an additional 38.5 GW between 2035 and 2047.

Furthermore, another report by CEA titled Long-Term National Resource Adequacy Plan for FY27–FY37 outlines a 30 GW expansion in hydropower capacity over the next decade. Subtracting the Brahmaputra Basin’s near-term targets, it is highly probable that approximately 10 GW of this capacity will be distributed across northern and southern river basins.

Patel Engineering: Aligning with the Hydropower and Pumped Storage Expansion

Patel Engineering: Business Overview

Patel Engineering is one of India’s premier hydroelectric EPC players, boasting a legacy of over seven decades in the infrastructure industry. Over the years, the company has executed several landmark hydroelectric projects, including the prestigious Koyna and Srisailam projects.

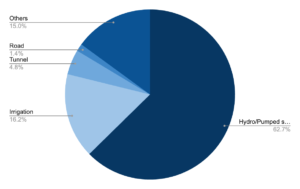

While Patel Engineering’s core focus lies in hydroelectric and pumped storage projects, the company also operates in complementary infrastructure verticals. Approximately 60% of its order book is concentrated in hydropower and PSPs, with the remainder comprising complex tunneling, irrigation, and other specialized civil works.

Source: Company data (Figure: 10)

Industry Overview

In India, only a limited number of engineering firms possess the execution track record required to construct large-scale (25 MW+) hydroelectric power plants. Consequently, the industry is characterized by a moderately concentrated structure consisting of fewer than ten major players. Key competitors include Larsen & Toubro (L&T), Megha Engineering, Patel Engineering, Afcons Infrastructure, and Hindustan Construction Company (HCC), alongside smaller, emerging contractors.

The majority of India’s hydropower projects are owned and managed by central PSUs, including NHPC, SJVN, and NEEPCO (a subsidiary of NTPC). These PSUs award construction contracts through competitive tenders, which are typically split into two distinct packages: civil works and hydro-mechanical construction. Patel Engineering primarily focuses on the specialized civil construction segment of these contracts.

Unlike traditional utility-scale hydropower, recent PSPs are also open to private developers. While these private players often possess their own in-house EPC arms, the highly complex civil works are typically subcontracted to specialized players like Patel Engineering.

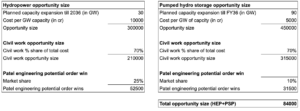

Opportunity Size

Based on our estimates, the combined opportunity size for Hydroelectric Projects and PSPs in India stands at a massive ₹7.5 lakh crore. Of this addressable market, Patel Engineering is well-positioned to target approximately ₹84,000 crore in order inflows over the medium term.

Source: Management comment, Strategic Alpha estimates. (Figure: 11)

Besides the hydropower and pumped storage opportunity, which currently accounts for 60% of the company’s total order book, Patel Engineering is poised to benefit from other developmental segments as well. Most notably, the company possesses specialized expertise in underground tunneling, which management estimates represents a medium-term opportunity size of ~₹1 lakh crore. This segment is being heavily driven by the government’s push to enhance strategic connectivity in remote mountainous and border areas.

Why Patel Engineering Stands Out as a Better play

Among listed peers with substantial exposure to the hydropower and PSP EPC space, Patel Engineering stands out as a highly compelling player. This is primarily due to its pure-play sector concentration, comfortable leverage, and deeply discounted valuations.

Source: Screener (Figure: 12)

Key Risks and Mitigating Factors

Undervalued equities typically carry specific operational overhangs, and Patel Engineering is no exception. From an industry perspective, hydropower and pumped storage developments feature long gestation periods and a myriad of execution variables, ranging from complex geological challenges to socio-environmental hurdles. Historically, extensive project delays have plagued the sector, causing working capital to lock up in unpaid receivables, which historically pushed several EPC companies into financial distress.

Another risk specific to Patel Engineering is potential market share erosion in the rapidly growing PSP segment. Historically, the majority of India’s utility-scale hydropower projects were commissioned by central PSUs, which systematically delegated civil construction works to specialized contractors like Patel Engineering. However, a significant portion of the upcoming PSP capacities has been allocated to private developers such as JSW Energy, Adani Green Energy, and Greenko. While these private conglomerates often maintain in-house EPC verticals, the extreme geological complexity of subterranean civil works makes it highly likely that they will continue to subcontract specialized tunneling and civil construction to experienced third-party EPC firms like Patel Engineering.

Closing Thoughts: Applying the FTVT Lens

India’s push for grid stability and the geopolitical imperative to secure border water rights are creating powerful macro tailwinds for the hydropower and Pumped Hydro Storage sectors.

Against this backdrop, Patel Engineering serves as a compelling case study to illustrate our FTVT framework in action. Operating as a specialized, pure-play hydropower EPC in an out-of-favor sector, the company effectively highlights the intersection of an emerging structural theme, improving fundamentals (characterized by low leverage), and a highly attractive valuation (~10x P/E). While the technical setup remains near-term subdued, we are monitoring the stock on our watchlist for a strong reversal setup on the chart.

While inherent industry risks like long gestation periods and private competition remain, this study demonstrates how we systematically identify and analyze neglected pockets of the market that are poised for a fundamental turnaround.

If you need guidance on how to start your stock market journey, how much capital is enough to begin with, how to do smart investing, or how to take informed stock market decisions, you can join Strategic Alpha’s ‘The Conviction Club’. This is a membership program, especially curated to help investors become aware and knowledgeable about stock market trends, news, and technical aspects, so that they can become their own experts.

Our YouTube channel, weekly webinars, and digital resources available on the website can help you learn the basics of the stock market. For regular updates on trends, one-to-one sessions with experts, and detailed learning modules, you can join the Conviction Club, which is the online community of like-minded investors sharing knowledge and thoughts to grow together.

Subscribe to the Strategic Alpha Newsletter now to get the latest updates about weekly webinars.

Join Me On My Telegram Channel Where I Share Much More Value Adding Knowledge Of Investing/ Trading: Click Here

Also, Don’t Forget To Follow Us On Our Social Media Accounts:

Facebook: https://www.facebook.com/strategicalpha/

Instagram: https://www.instagram.com/strategicalpha/

Twitter: https://twitter.com/suyog_dhavan

YouTube: https://bit.ly/2IIqztO

Disclaimer: Strategic Alpha and Suyog Dhavan are not SEBI-registered investment advisor. The content provided is purely for educational purposes and should not be construed as financial or investment advice. Viewers are encouraged to conduct their own research or consult with a SEBI-registered professional before making any investment decisions.