FOR YEARS, KASHMIR WAS THE RISK. WHAT IF IT BECOMES THE OPPORTUNITY?

A constitutional shift that changed more than politics – Revocation of Article 370

To understand Jammu & Kashmir Bank Ltd., you have to go back to Article 370, because for decades it shaped not just the politics of the region, but its economy, its institutions, and in many ways, its banking system.

Jammu & Kashmir did not evolve like the rest of India. After independence, when Maharaja Hari Singh signed the Instrument of Accession in 1947, the state became part of India, but with conditions. These conditions eventually took the form of Article 370, granting it a special constitutional status.

In practice, this meant the region functioned under a different economic and legal framework. Central laws did not automatically apply, property ownership was restricted, and policy integration with the rest of India was limited.

Over time, this created a gap.

While the rest of India went through infrastructure build-out, industrialisation, and financial deepening, Jammu & Kashmir remained relatively insulated, dealing with disturbances, lower private investment, and slower economic progress.

And this is where it starts to matter for the bank.

J&K Bank wasn’t just operating in a difficult market; it was operating in a structurally different economy.

Everything changed in August 2019.

The removal of Article 370 was a reset of the region’s economic framework. It opened the door to policy alignment, broader capital flows, and a more integrated growth path.

For the first time in decades, Jammu & Kashmir began moving closer to the mainstream economic trajectory of India.

Which brings us to the real question:

If the region itself is changing, what happens to a bank that is deeply rooted in it?

The financial backbone of the region

If Article 370 defined the economic boundaries of Jammu & Kashmir, then J&K Bank evolved within those boundaries and, over time, became central to them.

This isn’t just another regional bank.

Founded in 1938, J&K Bank has grown alongside the region itself. Today, it operates as a universal bank in J&K and Ladakh, while being more selective across the rest of India. But what truly sets it apart is how deeply it is embedded in the local ecosystem.

It is the primary banking partner to the government, and its reach cuts across segments: from farmers and small businesses to corporate and government employees. In many ways, it sits at the intersection of economic activity, public spending, and financial flows in the region.

That positioning has a direct implication: when the region grows, the bank doesn’t just participate, it reflects that growth.

Nearly 70% of its loan book is still anchored in its home territory, where it benefits from strong relationships, better pricing power, and a more stable deposit base. At the same time, the bank has built a second leg, expanding selectively in the rest of India to add scale without diluting risk.

This two-part structure is important.

The home market provides margins and depth, while the rest of India offers diversification and growth optionality.

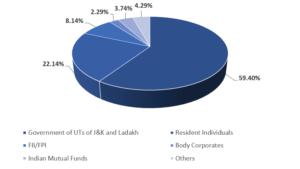

With majority government ownership and its role as banker to the UT, the bank enjoys a unique positioning that is difficult to replicate.

But for a long time, this strength came with a limitation.

The bank’s dominance in J&K also meant it was tied to a region that:

- saw limited private investment

- lagged in industrial development

- and remained heavily dependent on agriculture and government activity

Even today, with an economy of ~₹2.65 lakh crore and nearly 70% of the population linked to agriculture, the base is still evolving.

And that’s where the shift begins.

As the region opens up post-2019 – with better connectivity, rising investment, and improving economic activity – the same deep integration that once constrained the bank now starts to work in its favour.

This is not just a bank operating in a region, it is a direct proxy to how that region evolves.

And that changes how you look at its growth.

When everything went wrong: Governance, stress, and survival

To understand the bank’s turnaround, you have to look at how deep the problems actually were.

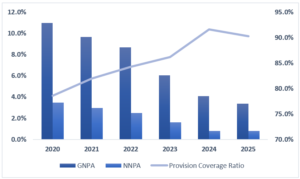

By FY19, J&K Bank was carrying a GNPA of ~10.5% and NNPA of ~4.9%. This wasn’t a cyclical uptick but a result of years of poor underwriting and weak credit discipline.

But the real issue ran deeper than asset quality.

Around 2019, serious governance concerns came to the surface. There were allegations of:

- loans being extended to politically connected borrowers

- aggressive and questionable one-time settlements

- inefficient capital allocation, including non-core spending

This eventually led to a management overhaul, with tighter oversight and a clear shift toward accountability.

At the same time, the external environment wasn’t helping.

The bank had to absorb a ~₹1,300 crore exposure to IL&FS, which required ~₹700+ crore provisioning. Soon after, COVID disrupted borrower cash flows, especially in sectors like tourism and small businesses that are critical to the region.

And unlike most banks, J&K Bank had very little insulation.

Its balance sheet was closely tied to a single geography that was dealing with:

- economic transition post-Article 370

- periodic disruptions and security concerns

- and a limited private sector base

So, stress didn’t come from one place. It came from everywhere.

Weak underwriting, governance lapses, and a fragile operating environment, all colliding at once.

But this is also what forced the reset.

With J&K becoming a Union Territory, the bank moved under tighter central and regulatory oversight. The earlier flexibility gave way to discipline, scrutiny, and standardisation.

What followed was not gradual improvement.

It was a forced recognition of stress, a clean-up of the loan book, and a rebuilding of governance from the ground up.

And that’s what makes this phase important.

Because the recovery you see today is not built on optimism, it is built on a hard reset after everything that could go wrong, did.

The hard reset: Cleaning up years of excess

What followed was a deliberate clean-up.

Over the last few years, J&K Bank has moved from recognising stress to actively resolving it, and the impact is visible in the numbers. GNPA has declined from ~10.5% to ~3%, but more importantly, the quality of the balance sheet has changed.

Early signs of stress have reduced, the pipeline of potential NPAs has come down, and with provision coverage at ~90%+, most of the legacy risk has already been absorbed.

This is not just about lower NPAs, it’s about control over future stress.

The approach taken during this phase has been disciplined. The bank focused on:

- recovering legacy accounts

- upgrading exposures wherever possible

- and recognising problems upfront rather than deferring them

A meaningful part of profitability during this period came from recoveries and provision write-backs, which is typical of a clean-up cycle. But here it reflects execution rather than accounting.

Just as important is what the bank chose not to do. It didn’t try to grow its way out of trouble.

Instead, the focus remained on stabilising the balance sheet, tightening credit filters, and improving internal processes. Underwriting became more standardised, monitoring sharper, and credit decisions more disciplined. And with a largely fixed cost base, incremental growth from here has the potential to improve efficiency and returns.

The outcome is now visible:

- slippages are under control

- credit costs are negligible

- earnings are far less volatile

And all of this has happened in a very different regulatory environment, post Article 370, where oversight is tighter and governance expectations are higher.

So today, the bank has moved into a much more steady-state.

The balance sheet is largely clean, processes are more disciplined, and the operating environment is improving. This is not a recovery in progress anymore; it is a reset that has already played out.

What matters now is not the clean-up, but what the bank does with this base.

Growing differently this time: Discipline over aggression

What’s changing now is not just the pace of growth, but the approach to it.

After years of focusing on clean-up, the bank has clearly shifted toward expansion. But unlike the previous cycle, growth is not being chased, it is being paced and filtered.

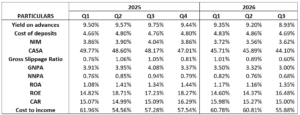

Even with credit growth running at ~17% YoY as of Q3 FY26, the bank continues to guide for ~12%, largely because deposit growth is lower. That decision is telling.

Growth is now being aligned with funding, not pushed ahead of it.

This is a clear departure from the past, where growth often came at the cost of asset quality.

There is also a structural shift in where this growth is coming from.

The bank is gradually building a more balanced mix, expanding in the rest of India while retaining its strength in the home market. The core geography continues to provide higher-margin, relationship-driven business, while the rest of India adds scale and diversification.

At a segment level, the strategy is equally deliberate.

Retail remains the anchor, while corporate lending is being approached with caution, focused largely on high-rated borrowers. The idea is simple: use retail to support margins, and corporate to build volumes without taking disproportionate risk.

This reflects a broader change in mindset.

The bank is no longer optimising for size; it is optimising for quality of growth.

At the same time, management is realistic about constraints.

Deposit growth is trailing credit growth, and the shift from CASA to term deposits is visible across the system. Instead of stretching the balance sheet, the focus has been on strengthening the liability franchise, especially through retail CASA in rest of India and deeper engagement in its core markets.

Margins, too, are being managed with discipline. Despite a 125-bps rate cut cycle, NIMs have held at ~3.6–3.7%, largely due to mix rather than pricing.

To support the next phase of credit growth, the bank is looking to raise around ₹1,500 crore of additional capital through a mix of Tier 2 bonds (~₹500 crore) and a subsequent QIP. This is important, as it ensures that growth is backed by capital and not constrained by it as the balance sheet scales. The timing of the QIP will depend on market conditions.

So, when you step back, the change is quite clear.

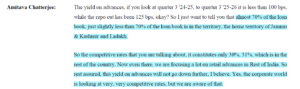

This shift also comes with a change in leadership. Amitava Chatterjee, who took over as MD & CEO in December 2024, brings over three decades of experience across business, risk, and large corporate relationships from SBI and SBICAPS, adding depth to the bank’s next phase of growth.

The bank is growing, but in a way that is funded, diversified, and risk-aware. It is not trying to be faster. It is trying to be better.

And that distinction will matter much more in the next phase.

For the first time in decades, the region itself is no longer the constraint.

To understand what lies ahead for J&K Bank, you have to step outside the bank and look at the region it operates in.

Because for the first time in decades, Jammu & Kashmir is not just stabilising, it is entering a growth phase.

The numbers are beginning to reflect that shift. The economy is estimated at around ₹2.65 lakh crore, with a growth of ~7% and projections of ~9.5% going forward. For a region that has historically lagged, this is a meaningful change in trajectory.

But more than the numbers, it’s the underlying drivers that matter.

Connectivity is improving in a way that directly impacts economic activity. The rail link to the rest of India is expected to ease long-standing logistical constraints thereby reducing costs, improving supply chains, and supporting both trade and tourism.

At the same time, the structure of the economy is gradually evolving.

While agriculture still supports a large part of the population, there is visible momentum in tourism, small businesses, and local entrepreneurship. Economic activity is becoming more broad-based, which is critical for sustained credit demand.

There is also a shift in sentiment.

Normalisation of daily life, improved participation in economic activity, and rising investor interest are all early indicators of a region moving toward greater stability and confidence. Incidents like the Pahalgam attack remind you that risks haven’t fully disappeared, but they no longer define the trajectory.

Policy support is reinforcing this shift.

Infrastructure spending, focus on connectivity, and initiatives aimed at improving industrial and power capacity are gradually building the foundation for higher economic activity. Given the relatively low base, even incremental improvements can have a disproportionate impact.

The government has invested ₹10,516 crore in the union territory of Jammu & Kashmir since 2019.

Now bring this back to the bank.

A large part of J&K Bank’s business is still anchored in this region. So, when the economy expands from ₹2.65 lakh crore toward ₹2.88 lakh crore, it directly translates into higher demand for credit, stronger deposit mobilisation, and deeper financial penetration.

For years, the region limited the bank’s growth.

Now, it is beginning to expand.

And that’s a very different starting point for what comes next.

After years of volatility, the numbers have finally stopped surprising

If you look at J&K Bank today, what stands out is not rapid growth but stability.

And that itself marks a shift.

The bank is now operating at a level where most key metrics have settled into a predictable range. Profitability is steady, asset quality is under control, and earnings are no longer volatile.

Return ratios reflect this. Return on assets is in the range of about 1.2% to 1.3%, while return on equity is around 15% to 16%. These are not peak numbers driven by one-time gains. They represent a more normalised earnings profile after the clean-up phase.

Margins have held up better than expected. Even after a 125-basis point rate cut cycle, net interest margins remain around 3.6% to 3.7%. This suggests that the bank has managed its loan mix and funding costs with reasonable discipline.

On asset quality, the improvement is now visible and sustained. Gross NPA is close to 3%, while net NPA is below 1% at about 0.7%. Provision coverage remains strong at over 90%, which reduces the risk from the existing book. More importantly, fresh stress formation has slowed, making the current position more stable than cyclical.

This is also reflected in credit costs, which have remained very low in recent quarters. While these may normalise slightly over time, the current trend indicates a low stress operating environment.

Growth is present but measured. Advances have grown at about 17% year on year, but the bank continues to guide for around 12%, given that deposit growth is closer to 10%. The loan to deposit ratio has moved up to about 72%, with some room to expand further in a controlled manner.

On the liability side, there has been some moderation. The CASA ratio is around 44%, reflecting broader industry trends where savings are moving toward higher yielding instruments. However, in the core geography, CASA remains stronger and continues to support funding costs.

Costs are broadly under control. Operating expenses have grown modestly, and employee costs are expected to remain contained due to retirements and replacement with lower cost hires over time.

There have been a few one-off impacts, such as provisions worth ₹180 crore linked to the Ellaquai Dehati Grameen Bank amalgamation and ₹68 crore on account of the Special Rehabilitation Package 2025. But these have not altered the underlying trajectory.

So, when you step back, the picture is fairly straightforward.

The bank is not in a recovery phase anymore. It is also not chasing aggressive growth.

It is operating in a steady state, with clean asset quality, stable profitability, and controlled expansion.

And that is a far stronger position than where it was just a few years ago.

The story is not without risks though. The bank remains geographically concentrated, deposit growth is still lagging, and any slowdown in the region’s economic momentum could directly impact performance.

What could go wrong?

The story has improved, but it is not without risks.

The most obvious one is geographic concentration. A large part of the bank’s business is still tied to Jammu & Kashmir, which means any disruption in the region can directly impact performance. Events like the Pahalgam attack are reminders that this risk still exists.

On the liability side, deposit growth is lagging credit growth, and CASA has moderated to ~44%. If this continues, the bank may have to rely more on higher-cost funding, which could put pressure on margins.

There is also the question of asset quality sustainability. Credit costs are currently very low due to the clean-up cycle, but as growth picks up, they are likely to normalise toward 20–30 bps. The real test will be maintaining discipline during expansion.

Execution outside the home market is another factor. Growth in the rest of India brings diversification, but also exposes the bank to more competitive markets where it lacks the same franchise strength.

Finally, the broader story still depends on the region’s economic trajectory. The improvement is visible, but still evolving, and any slowdown in activity could delay the expected growth.

At this stage, the risks are less about the past and more about execution from here.

So, the real question now is not if it can recover, but what it can become from here.

At this point, the story is no longer about recovery.

That phase is behind.

What matters now is whether the bank can take this stability and turn it into something more durable.

Because the setup is quite different today.

The balance sheet is clean. Asset quality is under control. Growth has returned, but it is being paced. The operating environment in the region is improving. And the bank is no longer constrained in the way it once was.

Individually, each of these is positive. Together, they create an opportunity.

But this is also where the nature of the story changes.

Until now, the bank has been driven by clean up and correction. Going forward, it will be judged on execution.

Can it improve its liability franchise as competition for deposits increases?

Can it maintain asset quality as the book expands?

Can it translate steady growth into better efficiency and stronger returns over time?

These are not structural problems. They are execution questions.

And that is an important distinction.

Because once a bank reaches this stage, the outcomes depend less on what went wrong in the past and more on how consistently it delivers from here.

The broader environment is supportive. Credit demand remains healthy across retail, agriculture, and small businesses. The region itself is entering a more stable growth phase. And the bank’s strategy is aligned with both.

Which means the direction is not uncertain.

The pace, however, will be.

So, the way to think about J&K Bank today is fairly simple.

This is no longer a story about fixing what was broken.

It is a story about proving what is possible.

And that proof will come not from one quarter or one year, but from how consistently the bank executes from here.

At Strategic Alpha, our aim is not just to track stories like Jammu & Kashmir Bank, but to thoroughly understand the thinking behind them. Because staying informed is important for investors. Stay connected for such detailed analysis of companies or become a part of our Conviction Club to grow along with several other like-minded investors.

If you need guidance on how to start your stock market journey, how much capital is enough to begin with, how to do smart investing, or how to take informed stock market decisions, you can join Strategic Alpha’s ‘The Conviction Club’. This is a membership program, especially curated to help investors become aware and knowledgeable about stock market trends, news, and technical aspects, so that they can become their own experts.

Our YouTube channel, weekly webinars, and digital resources available on the website can help you learn the basics of the stock market. For regular updates on trends, one-to-one sessions with experts, and detailed learning modules, you can join the Conviction Club, which is the online community of like-minded investors sharing knowledge and thoughts to grow together.

Subscribe to the Strategic Alpha Newsletter now to get the latest updates about weekly webinars.

Join Me On My Telegram Channel Where I Share Much More Value Adding Knowledge Of Investing/ Trading: Click Here

Also, Don’t Forget To Follow Us On Our Social Media Accounts:

Facebook: https://www.facebook.com/strategicalpha/

Instagram: https://www.instagram.com/strategicalpha/

Twitter: https://twitter.com/suyog_dhavan

YouTube: https://bit.ly/2IIqztO

Disclaimer: Strategic Alpha and Suyog Dhavan are not SEBI-registered investment advisor. The content provided is purely for educational purposes and should not be construed as financial or investment advice. Viewers are encouraged to conduct their own research or consult with a SEBI-registered professional before making any investment decisions.