IS INDIA BECOMING A HUB OF PHARMACEUTICAL INNOVATION?

For decades, the global pharmaceutical industry looked at India through a very specific lens.

If affordable medicines needed to reach millions of patients around the world, chances are they were manufactured in India. Over the years, Indian pharma companies have built deep capabilities in producing generic drugs at scale, supplying healthcare systems across both developed and emerging markets.

Today, India has firmly established itself as a cornerstone of the global pharmaceutical supply chain. The country ranks 3rd globally in pharmaceutical production by volume and 14th by value, and the sector has grown steadily, expanding at roughly 9.4% annually over the past decade. The industry now contributes close to 1.7% of India’s GDP.

But the real story becomes even clearer when we look at global healthcare programs.

A large share of the vaccines distributed through global initiatives originates in India. The country supplies more than half of UNICEF’s vaccine requirements, fulfills almost the entire global demand for WHO’s DPT vaccines, and produces a substantial share of BCG and measles vaccines used worldwide. Indian companies also manufacture over 80% of the antiretroviral medicines used globally to treat HIV/AIDS.

These numbers explain why India is often called the “pharmacy of the world.”

And it is not just a handful of companies driving this ecosystem. The domestic industry includes roughly 3,000 pharmaceutical firms and over 10,000 manufacturing facilities, supported by a large network of scientists, engineers, and manufacturing specialists.

Yet, a broader question is beginning to emerge.

Is India’s pharmaceutical industry entering a new phase?

Capital is flowing into the sector:

One signal that often gets overlooked in pharmaceutical analysis is where capital is flowing.

In recent years, the Indian pharma and healthcare sector has seen a steady rise in investment activity. In Q3 2025 alone, deal activity touched nearly ₹29,992 crore, with private equity and strategic acquisitions accounting for the bulk of transactions across dozens of deals. Earlier in the year, the sector recorded 71 deals worth around ₹22,279 crore in a single quarter.

This surge in capital suggests that investors are increasingly viewing India not just as a low-cost manufacturing hub, but as a growing innovation ecosystem in pharmaceuticals and biotechnology.

Government initiatives such as the Production Linked Incentive (PLI) scheme for pharmaceuticals and medical devices, the ₹5,000 crore Scheme for Promotion of Research and Innovation in Pharma, and the establishment of the Anusandhan National Research Foundation (ANRF), are all aimed at strengthening India’s research and manufacturing capabilities.

Together, these developments point toward a broader shift. India is gradually building the institutional support needed to move from generic drug manufacturing toward research driven pharmaceutical innovation.

For decades, India’s competitive advantage has been cost-efficient manufacturing. But the global pharma market is evolving. Many of the most important drugs today are no longer simple chemical formulations. Increasingly, treatments are shifting toward complex biologics.

This transition is where things get interesting.

However, we first need to understand why biologics are becoming one of the most important segments of modern healthcare.

THE RULES OF THE GAME ARE CHANGING

For decades, the pharma industry operated with a fairly simple rhythm.

A company would discover a drug, spend years bringing it through clinical trials, secure patent protection, and then sell it at high margins. When the patent expired, generic manufacturers would step in and produce cheaper versions, expanding access to millions of patients.

However, healthcare systems around the world are starting to question whether this model is sustainable.

Costs are rising sharply. Populations are aging. Chronic diseases like cancer, diabetes, and autoimmune disorders are becoming more common. Governments, insurers, and healthcare providers are all asking the same question:

How do we deliver better healthcare without letting costs spiral out of control?

And this question is quietly reshaping the expectations from pharma companies.

The industry is expected to help reduce the overall burden of disease—through earlier diagnosis, more precise treatments, digital monitoring of patients, and therapies that improve long-term outcomes.

If this transition is successful, pharma companies will be judged differently.

A new layer of global competition:

At the same time, another shift is happening in the background.

The Biosecure Act passed in the US in 2025, places restrictions on federal agencies from engaging with biotechnology equipment or services associated with certain foreign companies deemed to pose strategic risks. The intention is to protect sensitive biological and genomic data, while also reducing dependence on a narrow set of global supply chains.

What does this mean for the industry?

Pharmaceutical companies that once concentrated their research and manufacturing partnerships in a few regions may now need to diversify their supply chains.

And that opens up new opportunities.

This is where biologics change the equation:

Some of the most powerful therapies developed over the past two decades are biologic drugs—treatments derived from living cells rather than chemical synthesis.

These medicines are used to treat complex conditions and are also among the most expensive drugs in the world.

But like all drugs, biologics eventually lose patent protection.

When that happens, a new category of medicines enters the market: biosimilars.

These are highly similar versions of the original biologic drugs, designed to deliver the same therapeutic effect but at significantly lower costs.

And this is where the story becomes interesting.

Unlike traditional generics, biosimilars are much harder to develop and manufacture. The science is more complex, regulatory approvals take longer, and production requires specialized infrastructure.

Which means only a limited number of companies globally have the capability to compete in this space.

Among Indian pharma companies attempting this shift, Biocon Ltd has quietly built one of the most comprehensive platforms in biologics and biosimilars.

But to really understand where Biocon fits into this landscape, we need to take a closer look at the structure of the biologics industry itself.

WHERE IS PHARMA ACTUALLY GROWING?

There’s another way to look at this evolving industry. Just follow the growth.

For a long time, the pharmaceutical industry revolved around small-molecule drugs — the pills and tablets produced through chemical synthesis. These drugs built the modern generics industry.

But when we look at where the industry is growing today, the picture begins to change.

Small-molecule drugs are still expanding, but at a modest pace — roughly 2–4% annually.

Biologics, on the other hand, are growing three to four times faster, with projected growth of around 10–11% a year over the rest of the decade.

A market that keeps expanding:

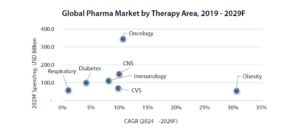

As the chart shows, global pharmaceutical spending has already crossed $1.1 trillion, and projections suggest it could approach $1.6 trillion by the end of the decade.

Source: Annual Report FY25, Biocon Ltd.

What’s interesting is not just the size of the market, but where that growth is concentrated.

Source: Annual Report FY25, Biocon Ltd.

Some of the fastest-expanding therapy areas today include oncology, immunology, metabolic disorders, and obesity treatments — all segments where biologics dominate the treatment landscape

Which means the next decade of pharmaceutical growth will likely be shaped less by traditional chemical drugs and more by complex biological therapies.

The opportunity that follows patent expiry:

Think of biosimilars as the biologics equivalent of generics.

But because biosimilars require deeper level of expertise and capabilities, the barriers to entry are much higher; which is why only a limited number of companies compete in this market.

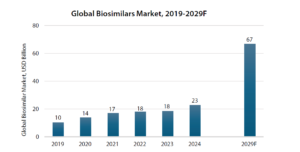

A market just getting started:

The global biosimilars market has already expanded from roughly $10 billion in 2019 to more than $20 billion today, and it could approach $60–70 billion by the end of the decade.

Hence, the opportunity ahead is substantial.

Source: Annual Report FY25, Biocon Ltd.

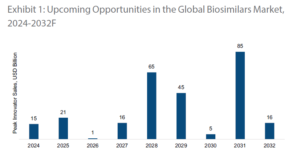

Over the next several years, biologic drugs with hundreds of billions of dollars in annual peak sales are expected to lose exclusivity. Each of those patent expiries opens the door for biosimilar competition.

Source: Annual Report FY25, Biocon Ltd.

Which means the next decade could see a wave of new biosimilar launches across major therapy areas.

And this is where strategy begins to matter:

Success in biosimilars requires:

- strong research capabilities

• complex biologics manufacturing

• regulatory expertise across multiple geographies

• and global commercialization networks

Only a handful of companies globally have managed to assemble all these pieces.

One of them is Biocon Ltd.

But before we look closely at Biocon’s strategy, it helps to ask a simpler question: who actually dominates the biosimilars market today?

THE GLOBAL RACE TO BUILD BIOSIMILAR PLATFORMS

Biosimilars follow a very different playbook and that complexity dramatically narrows the field.

To launch a biosimilar in major markets such as the US or Europe, companies must demonstrate that their product is highly similar to the original biologic, both in structure and clinical performance.

This takes time, capital, and experience.

Which is why the biosimilars market has evolved into something closer to an oligopoly of specialized players, rather than the fragmented landscape seen in traditional generics.

Global peers — competing in the biosimilar race:

| Company | Strategic Strength | Approx. Scale |

| Sandoz | Pioneer in biosimilars with early EU approvals and strong regulatory track record | ~US$10B revenue |

| Amgen | Strong biologics manufacturing and US commercialization power | ~US$35B |

| Samsung Bioepis | Rapid pipeline expansion through global partnerships | 9+ biosimilars approved globally |

| Celltrion | First company to commercialize monoclonal antibody biosimilars globally | Presence in 100+ countries |

| Biocon Ltd | Integrated biologics manufacturing with growing global distribution through Biocon Biologics Ltd. | Biosimilars revenue ~US$1B+ |

What makes this comparison interesting is the difference in business models.

Most global biosimilar leaders rely heavily on large commercial networks and partnerships, while Biocon has focused on building end-to-end biologics capabilities, which could become increasingly valuable as biologic supply chains diversify.

From volume to value: India’s quiet pharma advantage:

India today supplies roughly 20% of the world’s generic medicines, meeting nearly 40% of generic demand in the US and about 25% of medicines used in the UK. But as pricing pressure in generics intensifies, many Indian pharma companies are gradually moving up the value chain.

Across the industry, firms are investing in biologics, complex generics, and advanced manufacturing capabilities. Aurobindo Pharma has committed about ₹1,000 crore to build a biologics facility through a partnership with Merck, while Gland Pharma is expanding its GLP-1 manufacturing capacity from 40 million to 140 million units. At the same time, companies like Aurigene and Divi’s Laboratories are investing in cell therapy research and advanced intermediates manufacturing.

What makes this transition possible is the foundation India already possesses. The country has built deep strengths in process chemistry, large-scale manufacturing, regulatory compliance, and cost-efficient production, with hundreds of facilities approved by regulators such as the USFDA and WHO. Investment activity and government initiatives supporting research, bulk drug parks, and life sciences infrastructure are further strengthening this ecosystem.

Taken together, these trends suggest a broader shift—marking the next phase of India’s pharmaceutical evolution.

So where does Biocon fit in this scenario?

BUILDING A GLOBAL BIOLOGICS PLATFORM

If the biologics opportunity is as large as industry data suggests, a natural question follows: how can a company from India compete in a market dominated by global pharmaceutical giants?

For Biocon, the answer has been a gradual evolution. Founded in 1978 by Kiran Mazumdar Shaw as an enzyme manufacturer, the company steadily moved up the pharmaceutical value chain—from industrial enzymes to active pharmaceutical ingredients, and eventually into complex biologics.

Source: www.biocon.com

But developing biosimilars was only half the challenge. Indian companies long faced a structural hurdle: global commercialization. Without strong distribution networks and regulatory experience across major markets, even a strong pipeline could struggle to reach patients.

Biocon bridged this gap through partnerships with companies like Mylan, later part of Viatris, gaining access to regulated markets and building global credibility.

Those collaborations opened the door. But to compete at scale, the company would eventually need something more.

A transformational deal:

The real inflection point came in 2022, when Biocon Biologics Ltd. acquired the global biosimilars business of Viatris Inc.

For Biocon, this was not just another acquisition.

Suddenly the company was no longer just a developer of biosimilars. It had become a company capable of developing, manufacturing, and commercializing biologic medicines across multiple regions.

THE ARCHITECTURE OF BIOCON LTD. BUSINESS

Building biosimilars is one challenge. Building a profitable global biosimilars business is another.

A business built on multiple engines

Source: Annual Report FY25, Biocon Ltd.

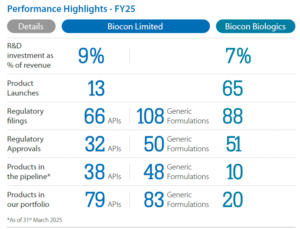

At the center sits the parent company, Biocon Ltd, which now integrates both generics and biosimilars operations across more than 120 countries.

Together, Biocon’s businesses create a structure that spans the entire pharmaceutical value chain:

Research and discovery → Process development → Manufacturing → Commercialization

Few companies in emerging markets operate with this level of integration.

In biologics, where production involves complex processes like fermentation, cell line development, and purification, this level of integration matters.

Controlling more stages of the process can help reduce development costs, accelerate product launches, and scale manufacturing more efficiently.

Source: www.biocon.com

Building the platform

Over the past few years, Biocon Ltd has been investing heavily behind the scenes to prepare for the next phase of growth.

Source: www.biocon.com

Between FY23 and FY25, capital expenditure steadily increased, peaking at about $274 million, as the company expanded monoclonal antibody facilities in India, strengthened insulin manufacturing capacity in Malaysia, and built new formulation capabilities across its network.

What is interesting is that this investment cycle now appears largely complete. Management has indicated that no major new capex projects are planned in the next couple of years, suggesting the infrastructure needed to support growth is already in place.

At the same time, the balance sheet is gradually stabilizing after the Viatris acquisition. Debt refinancing and structured instrument redemptions are expected to lower interest costs by roughly ₹300 crore from FY27

In other words, Biocon has spent the last few years building the platform. The real test now lies in how effectively it can scale it.

The next opportunity-GLP 1 therapies:

Another area that illustrates this model is the emerging market for GLP 1 therapies, used in diabetes and obesity treatments.

GLP 1 therapies are not just about the molecule.

They are also about delivery devices, manufacturing scale, and supply chain capabilities.

According to management commentary, this is an area where Biocon believes it has a structural advantage, which allows it to participate not just in biosimilars but also in the broader opportunity around GLP 1 based therapies.

Consolidating the platform:

Recently the company also simplified its structure by integrating Biocon Biologics Ltd. more closely with the parent entity, moving toward a unified pharmaceutical platform that combines generics and biologics across global markets.

The objective is straightforward.

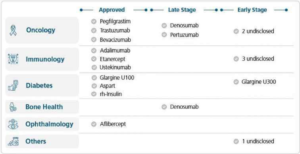

Through BBL, the company has already commercialised nine biosimilars across insulin, oncology, immunology and ophthalmology, including insulin glargine (Semglee), trastuzumab (Ogivri), pegfilgrastim (Fulphila) and bevacizumab (Abevmy). These products target markets worth tens of billions of dollars, and biosimilars now contribute roughly 60% of group revenue, providing visibility for the next several years.

Management has described this as an opportunity to unlock value through a simpler operating structure while leveraging common capabilities across the portfolio.

A small detail with big economics:

Through recent developments, Biocon now has full rights to the Hulio assets, a biosimilar version of Adalimumab, giving it greater control over commercialization and cost structure.

That matters because adalimumab has historically been one of the largest selling biologic drugs in the world. Even a modest share of the biosimilar market can translate into meaningful revenue.

When we step back and look at all these pieces together, a clearer picture begins to emerge.

But that still leaves one final question.

How strong are Biocon’s financial foundations to support this strategy?

The other pillars:

While biologics drive the long-term story, the rest of the company still plays an important role.

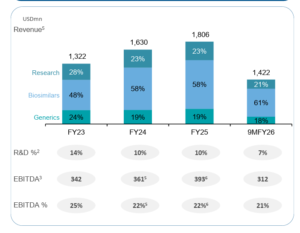

The generics business focuses on small molecule APIs and formulations. Margins here are lower compared to biologics, but the segment provides steady revenue and manufacturing scale.

Then there is Syngene International, the company’s research services (CRDMO) arm. Syngene works with global pharmaceutical companies on drug discovery, development, and contract research programs.

Within Biocon Ltd, the Novel Biologics segment represents the company’s long-term innovation engine. This segment focuses on developing new biological therapies for diseases with limited treatment options, particularly in areas such as metabolic disorders and autoimmune diseases. While this segment currently contributes a relatively small share of revenue, it reflects Biocon’s broader ambition to move beyond biosimilars and participate in original biologic drug discovery, positioning the company closer to global innovation-led pharma models.

The next phase: from integration to execution:

The Viatris biosimilars acquisition gave Biocon Ltd something it previously lacked: global commercial scale. It also increased leverage, pushing debt above ₹17,000 crore, but management has since begun stabilizing the balance sheet through refinancing and gradual deleveraging.

Source: Annual Report FY25, Biocon Ltd.

Now the focus shifts to execution.

As biosimilars scale in markets like the US and Europe, operating leverage could begin to emerge. Management expects margins to improve as the product mix shifts toward higher-value biologics in oncology and immunology, with EBITDA margins potentially moving toward the mid-to-high twenties over time.

Early signs are encouraging. Several biosimilars have already secured broad insurance coverage and formulary access in the US, while expansion into markets such as Brazil, China, and parts of the Middle East and Asia is opening new growth avenues.

Source: Annual Report FY25, Biocon Ltd.

The pipeline also suggests more momentum ahead. Over the next 12–18 months, broader uptake of recently launched biosimilars and new biologic launches could shape the next phase of growth.

In other words, the platform is built.

The question now is how quickly Biocon can convert it into commercial momentum.

WHY IS BIOCON INTERESTING… AND WHERE DO THE RISKS LIE?

If there is one thing that makes Biocon Ltd stand out, it is this: the company is trying to build something very few emerging market pharmaceutical firms have attempted—a global biologics platform.

Source: Annual Report FY25, Biocon Ltd.

The opportunity sits at the intersection of two major trends: the rise of biosimilars and the growing importance of complex biologics manufacturing.

But the path is not without risks. Biosimilars remain a highly competitive and price-sensitive market, while regulatory scrutiny and manufacturing complexity add another layer of challenge. The balance sheet also still reflects the Viatris acquisition, with debt remaining elevated.

Ultimately, Biocon’s story is not just about launching biosimilars.

It is about whether the company can turn scientific capability and global scale into sustainable profitability.

And that is what makes the next few years particularly interesting to watch.

THE LONG GAME

For decades, the pharmaceutical industry followed a simple pattern.

Innovation happened in the West. The manufacturing scale came from the East.

India mastered the second part, becoming the world’s largest supplier of generic medicines and vaccines.

But the next chapter may look different.

Biologic drugs are reshaping modern medicine, shifting the focus from producing medicines cheaply to engineering complex therapies at scale. Through its biologics platform, Biocon is attempting to participate in that shift.

This is a long game. Biologics businesses take years to build, with heavy investment and complex regulatory pathways.

Which makes the Biocon story less about quarterly numbers and more about industrial ambition.

The question is no longer whether India can manufacture medicines for the world.

The real question is whether companies like Biocon can help create the next generation of them.

Become a Part of The Conviction Club: Get Real Insights from Market Trends

At Strategic Alpha, we go beyond the headlines to find real insights from market trends and data. For more detailed analysis of such companies or sectors, become a part of our fastest-growing investors economy. After joining Conviction Club, you can connect with like-minded investors, receive guidance from our investment experts, and make better decisions.

If you need guidance on how to start your stock market journey, how much capital is enough to begin with, how to do smart investing, or how to take informed stock market decisions, you can join Strategic Alpha’s ‘The Conviction Club’. This is a membership program, especially curated to help investors become aware and knowledgeable about stock market trends, news, and technical aspects, so that they can become their own experts.

Our YouTube channel, weekly webinars, and digital resources available on the website can help you learn the basics of the stock market. For regular updates on trends, one-to-one sessions with experts, and detailed learning modules, you can join the Conviction Club, which is the online community of like-minded investors sharing knowledge and thoughts to grow together.

Subscribe to the Strategic Alpha Newsletter now to get the latest updates about weekly webinars.

Join Me On My Telegram Channel Where I Share Much More Value Adding Knowledge Of Investing/ Trading: Click Here

Also, Don’t Forget To Follow Us On Our Social Media Accounts:

Facebook: https://www.facebook.com/strategicalpha/

Instagram: https://www.instagram.com/strategicalpha/

Twitter: https://twitter.com/suyog_dhavan

YouTube: https://bit.ly/2IIqztO

Disclaimer: Strategic Alpha and Suyog Dhavan are not SEBI-registered investment advisor. The content provided is purely for educational purposes and should not be construed as financial or investment advice. Viewers are encouraged to conduct their own research or consult with a SEBI-registered professional before making any investment decisions.