To understand Sammaan Capital’s transformation today, it is important to revisit the events of 2018, when the collapse of Infrastructure Leasing & Financial Services (IL&FS) triggered one of the biggest liquidity crises in India’s financial sector.

IL&FS, a systemically important infrastructure financing conglomerate, defaulted on multiple debt obligations in 2018 despite carrying aggregate borrowings of nearly INR91,000 crore. The defaults sent shockwaves through India’s debt markets and led investors, banks and mutual funds to reassess the risks associated with Non-Banking Financial Companies (NBFCs) and Housing Finance Companies (HFCs). What initially appeared to be an isolated corporate default soon evolved into a sector-wide liquidity crisis.

Prior to the crisis, housing finance companies had enjoyed easy access to funding through bank borrowings, commercial paper and bond markets. However, after the IL&FS collapse, liquidity in the financial system tightened sharply. Mutual funds reduced their exposure to NBFC debt, lenders became increasingly selective, and funding costs across the sector rose materially. Several housing finance companies witnessed severe stock price corrections as investors questioned the sustainability of their business models and funding structures.

Among the companies caught in this industry-wide turmoil was Indiabulls Housing Finance, now known as Sammaan Capital. At the time, the company was one of India’s largest housing finance companies with assets under management exceeding INR1.1 lakh crore. Although the company remained adequately capitalised and continued to report relatively healthy asset quality, the market’s perception of housing finance companies changed dramatically following the IL&FS collapse. Growth slowed across the sector as access to wholesale funding became more challenging and investors began demanding stronger liquidity buffers

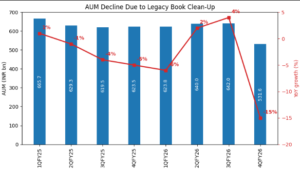

The IL&FS crisis exposed a structural weakness across many housing finance companies, including Sammaan Capital (then Indiabulls Housing Finance). The company largely funded long-tenure mortgage assets using wholesale borrowings with an average maturity of only 3–4 years, while its loan portfolio had an average maturity of more than 7 years. When liquidity evaporated after the IL&FS default, refinancing became difficult and lenders turned risk-averse. As a result, management shifted its priority from growth to survival, focusing on debt repayment, liquidity preservation, and balance-sheet deleveraging. Since September 2018, the company has repaid over ₹1.66 lakh crore of gross debt and more than ₹85,000 crore of net debt, while intentionally reducing AUM by over 50% to restore financial stability.

The second challenge was the legacy wholesale loan book, particularly real-estate developer exposures that came under stress during the prolonged funding slowdown and the COVID period. Rather than pursuing aggressive growth, management spent the next several years running down this book, strengthening provisions, and improving asset quality. Gross NPAs declined from crisis-era levels to below 3%, Stage-2 assets reduced from nearly 24% during the pandemic to below 5%, and the company accumulated provision buffers of over ₹9,500 crore against legacy risks.

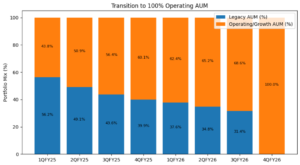

At the same time, it gradually built a retail lending franchise through co-lending partnerships, with co-lending and sell-down funded AUM increasing from roughly 10% in FY18 to more than 35% of AUM.

Sammaan Capital gradually shifted away from a balance-sheet-heavy wholesale lending model towards an asset-light retail franchise built around co-lending, direct assignments and mortgage origination. Under this model, the company not only earns interest spreads on the portion retained on its balance sheet but also generates additional income through origination fees, processing fees, securitisation gains and cross-sell opportunities. Since a significant portion of the loans are funded by partner banks, capital requirements and funding risks are substantially lower than under the traditional NBFC model.

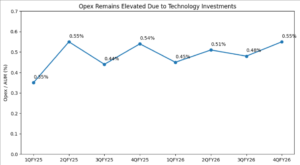

Over time, management expects profitability to benefit from multiple structural levers. These include lower credit costs due to the secured nature of retail mortgages, improved operating efficiency as branch productivity scales up, and a declining cost-to-income ratio through technology-led processes and operating leverage. Unlike the pre-2018 model, where growth was heavily dependent on balance-sheet expansion and leverage, the new strategy aims to generate higher ROA and ROE through fee income, faster asset churn, better capital efficiency and disciplined risk management. In essence, the company is attempting to build a platform-led lending franchise where earnings growth is driven not only by loan growth but also by improving productivity, recurring fee income streams and a structurally lower risk profile.

Business Transformation & Future Direction

Sammaan Capital appears to be at a pivotal stage in its transformation journey following the strategic investment by Abu Dhabi-based International Holding Company (IHC). The investment not only provides substantial growth capital but also marks the culmination of the company’s balance-sheet clean-up efforts, allowing management to shift its focus from asset-quality resolution to scalable growth.

IHC has committed a total investment of INR88.5 billion through its affiliate Avenir Investment RSC Ltd. Of this, INR56.5 billion has already been infused through equity issuance, while the remaining INR32 billion is expected to be received through warrant conversion over the next 18 months. Following the initial infusion, IHC holds a 28.5% stake in the company, which is expected to increase to 43.5% after the conversion of warrants. Beyond capital support, management believes the partnership will strengthen governance standards, improve access to funding, and accelerate the adoption of technology and AI-led capabilities across the lending platform.

The impact of the capital raise is already visible. CRISIL, CARE and ICRA have upgraded Sammaan Capital’s credit rating to AA+, while the company is also engaging with international rating agencies for further upgrades. Management expects that improved credit ratings, coupled with stronger relationships with lenders, should gradually reduce borrowing costs and help the company move closer to the funding profile enjoyed by the best-in-class housing finance peers.

Perhaps the most important milestone in the transformation has been the completion of the balance-sheet clean-up. The company has written off its legacy stressed assets and consolidated its business around an AUM of INR531.6 billion. As a result, the opening loan book now carries a zero-NPA position, eliminating the need for any incremental provisioning on legacy assets going forward. This marks a significant shift from the company’s past challenges and provides a much cleaner foundation for future growth. In addition, management expects recoveries of nearly INR70 billion from the fully provided legacy book over the coming years, creating a potential source of incremental value.

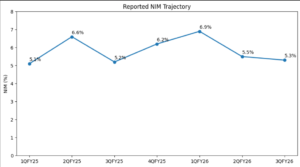

The current loan book generates a return on assets (ROA) of approximately 1.6%, which management believes provides sufficient earnings capacity to fund investments in technology, distribution expansion and talent acquisition. Over the medium term, the company is repositioning itself from a predominantly wholesale lender to a diversified retail-focused financial institution with a strong preference for secured lending.

Growth over the next few years is expected to be led by mortgages. Prime housing loans will largely be originated for sell-down to banks, while affordable housing and semi-urban mortgage loans will be retained on the company’s books. In commercial real estate (CRE), the company plans to adopt a co-origination model alongside credit funds under pari-passu structures, thereby limiting on-balance-sheet risk. Beyond its existing businesses, Sammaan Capital also intends to build scale in newer segments such as loan-against-securities and gold loans from FY27 onwards.

Management’s long-term vision is to build a highly diversified retail franchise, targeting 80% realisation of the balance sheet and an 80:20 mix between secured ,semi- secured and unsecured lending. While approximately 80% of disbursements over the next two years are expected to come from existing product segments, this share is projected to decline to around 50% by FY30 as newer lending verticals gain scale. The company also plans to follow an asset-light growth model, with nearly 30% of incremental disbursements expected to be routed through co-lending and direct assignment arrangements.

To support this expansion, Sammaan Capital plans to significantly strengthen its distribution and operating infrastructure, targeting a workforce of 20,000 employees and a branch network of 1,600 locations by FY30. At the same time, management aims to maintain a cost-to-income ratio below 30% through productivity improvements, digitisation and technology investments.

Importantly, the company intends to pursue growth while maintaining conservative risk parameters. Management has committed to keeping its capital adequacy ratio above 20%, maintaining leverage within 3.5x–4.0x, and preserving liquidity buffers equivalent to at least six months of repayments or 10-15% of total borrowings. With a cleaned-up balance sheet, a zero-NPA opening book, substantial capital support from IHC, improving credit ratings and a clearly defined strategy, Sammaan Capital appears to be transitioning from a turnaround story into the early stages of a sustainable growth phase.

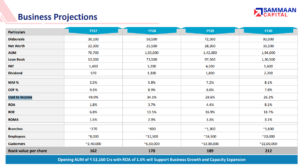

Business Projections By The Management

Strategic Outlook

- Legacy Issues Largely Behind the Company

- The legacy stressed book, which impacted profitability, asset quality, and investor sentiment for years, has been substantially resolved.

- The company starts FY27 with a largely clean book and ₹53,160 Cr AUM, allowing management to focus on growth rather than balance-sheet repair.

- Significant Profitability Improvement Potential

- Management targets ROA of 4–5% and ROE of 15–18% till 2030 vs current levels affected by restructuring and legacy provisions.

- As credit costs normalize and the business scales, earnings recovery could be meaningful.

- Aims to bring Cost to Income from 50% to 26% till 2030

- Funding Cost Reduction is a Major Earnings Lever

- The ₹8,850 Cr investment by IHC strengthens capital, governance, and access to technology.

- Management expects up to 160 bps reduction in cost of funds through rating upgrades from AA to AA+ over next 3 years and additional 100 bps AA+ to AAA and improved market access, which can materially boost margins.

- Business Model Transformation Reduces Risk

- The company is shifting from a wholesale-focused lender to an 80% retail-focused portfolio, with 60% secured and 20% semi-secured loans.

- This should improve portfolio granularity, reduce concentration risk, and enhance resilience across credit cycles.

- The FY30 target is to expand our workforce to 20,000 people, have a branch network of 1,600 branches and have over 15 products from current 1,956 employees and 218 branches & increase their loan per employee from 0.6 to 2.

- Value Assertive if Execution Delivers

- The company continues to be valued at around 1x P/B as recent profitability has been weighed down by legacy issues (ROE -3%, ROA 1.6%). As these legacy overhangs recede and the focus shifts toward growth, the market’s attention is likely to move from balance-sheet repair to earnings potential and execution.

- Successful execution of growth, asset quality, and funding-cost improvements could drive both earnings growth and valuation.

If you need guidance on how to start your stock market journey, how much capital is enough to begin with, how to do smart investing, or how to take informed stock market decisions, you can join Strategic Alpha’s ‘The Conviction Club’. This is a membership program, especially curated to help investors become aware and knowledgeable about stock market trends, news, and technical aspects, so that they can become their own experts.

Our YouTube channel, weekly webinars, and digital resources available on the website can help you learn the basics of the stock market. For regular updates on trends, one-to-one sessions with experts, and detailed learning modules, you can join the Conviction Club, which is the online community of like-minded investors sharing knowledge and thoughts to grow together.

Subscribe to the Strategic Alpha Newsletter now to get the latest updates about weekly webinars.

Join Me On My Telegram Channel Where I Share Much More Value Adding Knowledge Of Investing/ Trading: Click Here

Also, Don’t Forget To Follow Us On Our Social Media Accounts:

Facebook: https://www.facebook.com/strategicalpha/

Instagram: https://www.instagram.com/strategicalpha/

Twitter: https://twitter.com/suyog_dhavan

YouTube: https://bit.ly/2IIqztO

Disclaimer: Strategic Alpha and Suyog Dhavan are not SEBI-registered investment advisor. The content provided is purely for educational purposes and should not be construed as financial or investment advice. Viewers are encouraged to conduct their own research or consult with a SEBI-registered professional before making any investment decisions.